Wiemer Salverda

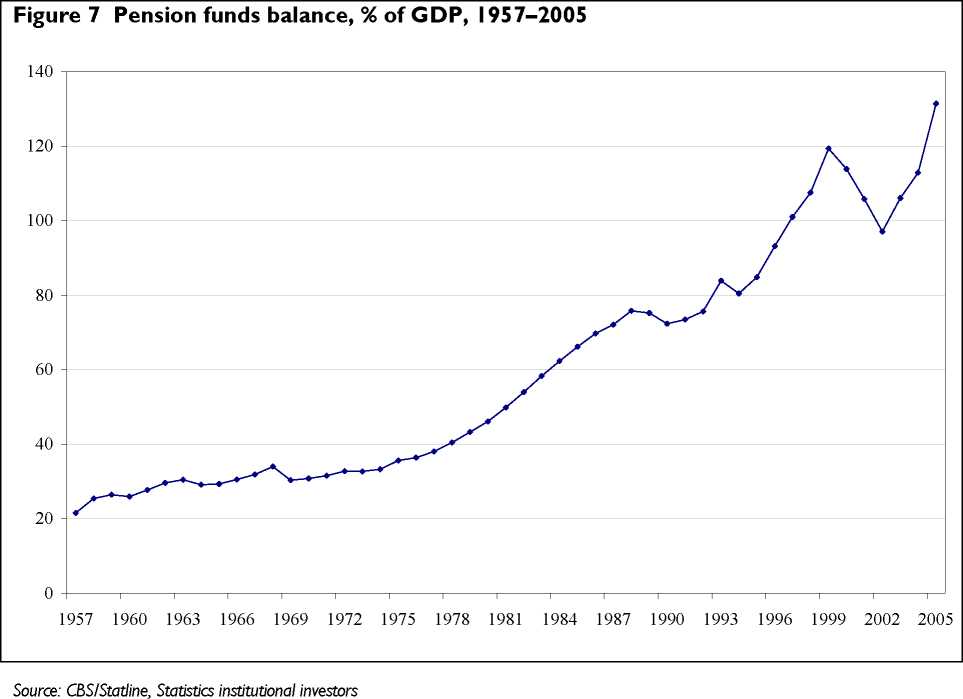

At the end of 2005 the book value of the pension funds corresponded to 130% of GDP. The

Netherlands ranks first in the world in this respect, together with Switzerland and Iceland.

Provisions for old age in many European countries are largely funded by pay-as-you-go systems. This

contrasts with the Anglo-Saxon countries where capital funding is the rule, but even there the

savings accumulated in capital funds are only half the size of what is found for the topranking

countries. Pay-as-you-go funding is not in itself a disadvantage; in a demographic steady state it can

even be more economical because it is much simpler - and hence cheaper - to administer and it is

not susceptible to fluctuating interest rates and share returns. The advantage of capital funding,

however, is that it can also benefit from revenue from investments abroad, where the demographic

situation may be more favourable. In addition to pay-as-you-go or capital funding, private savings

(and debt) are also important, but they are more difficult to measure and compare internationally.

Van Aggelen et al. (2006) state that countries like Italy have huge savings tied up in house ownership,

partly for the purpose of old age, and they also take debt - such as the high mortgage debt in the

Netherlands - into consideration, alongside pension savings. It should be noticed that the magnitude

of the pension funds is a mixed blessing because any erosion quickly becomes of considerable

magnitude in relation to the national economy. This was illustrated by the recent Dutch experience

after the dotcom bubble burst when aggregate pension savings fell by 20% of GDP. Any adjustments

24

AIAS - UvA

More intriguing information

1. Qualifying Recital: Lisa Carol Hardaway, flute2. Sectoral specialisation in the EU a macroeconomic perspective

3. Word searches: on the use of verbal and non-verbal resources during classroom talk

4. Explaining Growth in Dutch Agriculture: Prices, Public R&D, and Technological Change

5. Smith and Rawls Share a Room

6. Bridging Micro- and Macro-Analyses of the EU Sugar Program: Methods and Insights

7. ISSUES IN NONMARKET VALUATION AND POLICY APPLICATION: A RETROSPECTIVE GLANCE

8. The name is absent

9. THE MEXICAN HOG INDUSTRY: MOVING BEYOND 2003

10. La mobilité de la main-d'œuvre en Europe : le rôle des caractéristiques individuelles et de l'hétérogénéité entre pays