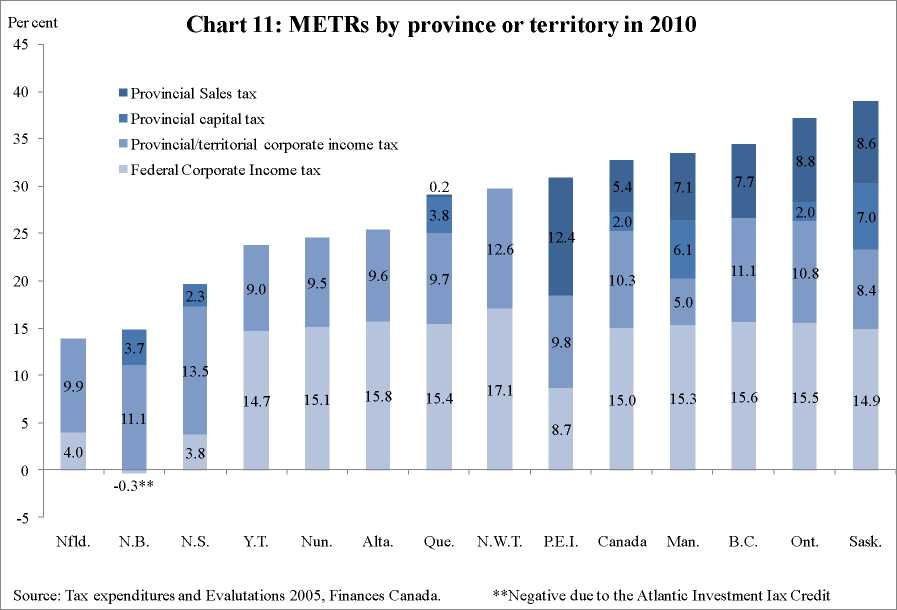

34

In the other five provinces, the PST has been merged with the GST (i.e. the

Harmonized Sales Tax (HST) in New Brunswick, Nova Scotia, and Newfoundland), or

replaced with a value added tax (Quebec), or never existed (Alberta). Chart 11 shows that

if there were no PST on the purchase of capital goods, the METRs in Canada in 2010

would be approximately 5 percentage points lower.

Tax policy experts across the political spectrum are unanimous that the current

PST regime which taxes the purchase of new capital equipment is extremely bad policy,

perhaps unique in its incompetence among developed countries.

The effect of such a tax is to increase the price of capital relative to the price of

labour, giving firms less incentive to substitute capital for labour and hence leading to

slower growth in the capital-labour ratio or capital intensity. Since capital intensity

growth is a key driver of labour productivity, the latter suffers. If Canada were a labour

surplus country, there might be some justification for such a policy on the basis of

fostering employment, at least in the short to medium term.23 But with the unemployment

rate at around 6 per cent, Canada should be encouraging substitution of capital for labour.

Evidence of the positive effect of the removal of the PST on capital investment

comes from work by Michael Smart and Richard Bird (2006) and Smart (2007). They

find that the growth in investment per capita has been more rapid in the HST provinces

that do not tax capital inputs than in PST provinces that impose such a tax. In an

23 It is however not clear that the long-run health of an economy is promoted by subsidizing employment

and taxing capital goods.

More intriguing information

1. Electricity output in Spain: Economic analysis of the activity after liberalization2. Sex differences in the structure and stability of children’s playground social networks and their overlap with friendship relations

3. The name is absent

4. Modellgestützte Politikberatung im Naturschutz: Zur „optimalen“ Flächennutzung in der Agrarlandschaft des Biosphärenreservates „Mittlere Elbe“

5. Who is missing from higher education?

6. THE MEXICAN HOG INDUSTRY: MOVING BEYOND 2003

7. Tissue Tracking Imaging for Identifying the Origin of Idiopathic Ventricular Arrhythmias: A New Role of Cardiac Ultrasound in Electrophysiology

8. Perfect Regular Equilibrium

9. Factores de alteração da composição da Despesa Pública: o caso norte-americano

10. GENE EXPRESSION AND ITS DISCONTENTS Developmental disorders as dysfunctions of epigenetic cognition