48 July 1989

N + 1

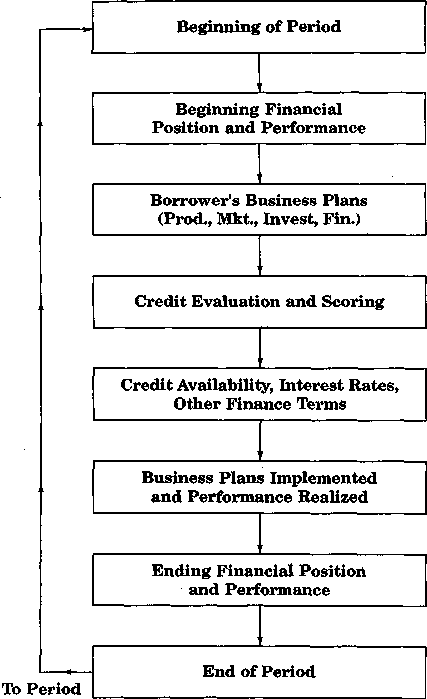

Figure 1. Credit evaluation process and loan

pricing

lender and borrower may modify the plans and

eventually agree on the availability of various

types of credit, the levels of interest rates, col-

lateral requirements, loan maturities, and oth-

er financing terms. The borrower then imple-

ments the business plans, carries on the firm’s

activities over the period, and realizes the re-

sulting performance. The ending financial po-

sition accounts for the combined effects of the

beginning position, the business plans, the

credit terms, and the subsequent outcomes.

Finally, the ending position becomes the be-

ginning position for the next period, in which

the process is repeated, and this sequence con-

tinues until the horizon is reached.

Methodology

The recursive process presented in the preced-

ing section could be implemented using sim-

ulation or optimization procedures. Optimi-

zation offers the opportunity to observe

Western Journal of Agricultural Economics

financial performance, investment patterns,

and financing activities that arise from the

firm’s efforts to push against its resource limits

and operating requirements in order to max-

imize the stipulated objectives. However, a

mathematical programming approach suffers

from difficulties in endogenizing a credit scor-

ing function in which the variables are ex-

pressed by financial ratios and from a less flex-

ible approach for testing the effects of

alternative investment strategies, parameter

specifications, and environmental conditions.

Accordingly, a recursive, multiperiod sim-

ulation model is formulated for use in this study

in order to portray the firm’s financial setting

and business opportunities. The model is for-

mulated, using the LOTUS 123 spreadsheet

software, as a series of annual business deci-

sions and performance results with integer

specifications on major business investments.

The periods are linked together by financial

transfers from one period to the next and by

the credit scoring procedure in which the firm’s

cost ofborrowing is determined by its financial

position at the end of the preceding period

which itself reflects the cumulative effects of

past performance. Thus, the model resembles

the basic approach of other commonly used

simulation models (Richardson and Nixon;

Walker and Helmers; Schnitkey, Barry, and

Ellinger), except for the annual updating of the

credit scoring and loan pricing mechanism, a

deterministic specification, and less empirical

detail on production and marketing compo-

nents.

A deterministic model is specified in order

to highlight the relationships among business

plans, financial performance, the credit score,

and borrowing costs. That is, values for gross

receipts, operating costs, growth rates, and oth-

er parameters are all expressed by single-val-

ued expectations. A stochastic framework

would add further realism, including the pro-

vision for alternative risk attitudes and meth-

ods of responding to risk; however, the added

complexities would obscure the key relation-

ships and might yield performance measures

(e.g., variance of income or wealth, probability

of loss, probability distributions) that are not

directly reflected in credit scoring procedures

used by lenders.

Model Components

The model’s components include the firm’s

initial financial position, operating decisions,

More intriguing information

1. The name is absent2. Comparative study of hatching rates of African catfish (Clarias gariepinus Burchell 1822) eggs on different substrates

3. POWER LAW SIGNATURE IN INDONESIAN LEGISLATIVE ELECTION 1999-2004

4. Keystone sector methodology:network analysis comparative study

5. The Economics of Uncovered Interest Parity Condition for Emerging Markets: A Survey

6. Chebyshev polynomial approximation to approximate partial differential equations

7. A NEW PERSPECTIVE ON UNDERINVESTMENT IN AGRICULTURAL R&D

8. School Effectiveness in Developing Countries - A Summary of the Research Evidence

9. The purpose of this paper is to report on the 2008 inaugural Equal Opportunities Conference held at the University of East Anglia, Norwich

10. The name is absent