The Interest Rate-Exchange Rate Link in the Mexican Float

together with the rates of inflation and currency exchange (pesos per

dollar; the series are precisely defined below, in Subsection IIc). There

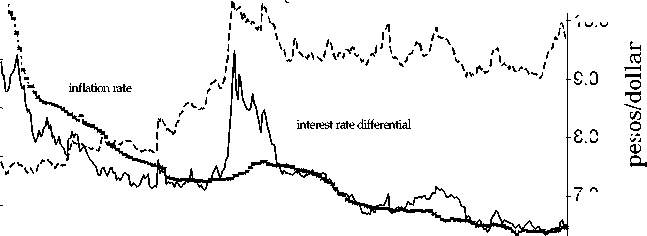

are two important observations to make: the first is that the interest

rate differential is strongly trended, and that the trend appears to be

determined by the inflation rate (with transitory departures caused

by phenomena such as the Russian crisis of August 1998). In terms of

Equation (1), this observation suggests that, in the long run, the

expected depreciation rate is determined by the domestic inflation

rate, perhaps because expected inflation is, to an important extent,

determined by current inflation.

60

Figure 1. Interest rate differential, and inflation and exchange rates.

11.0

exchange rate (rhs scale)

10.0

50 -%

40

30

20 -

10

9.0

8.0

co

7.0

6.0

010/04/1996 01/02/1997 31/12/1997 31/12/1998 30/12/1999 28/12/2000 27/12/2001

week

A second feature to note is the strong positive contemporaneous

correlation between the interest differential and the exchange rate,

presumably as a reflection of the presence of capital account shocks.7

In this case, an exogenous rise in the world demand for peso assets,

for instance, would simultaneously strengthen the currency and push

local interest rates down. This observation implies that any possibility

of finding a negative relationship will depend on including a long lag

7 It may be important to note that during this period the domestic interest rate under

study was not a direct instrument in the Banco de Mexico’s policy rule, but a market-determined

variable (subject, of course, to influence from central bank actions).

11

More intriguing information

1. The effect of globalisation on industrial districts in Italy: evidence from the footwear sector2. Une nouvelle vision de l'économie (The knowledge society: a new approach of the economy)

3. Sex-gender-sexuality: how sex, gender, and sexuality constellations are constituted in secondary schools

4. Equity Markets and Economic Development: What Do We Know

5. PROFITABILITY OF ALFALFA HAY STORAGE USING PROBABILITIES: AN EXTENSION APPROACH

6. Concerns for Equity and the Optimal Co-Payments for Publicly Provided Health Care

7. The name is absent

8. The name is absent

9. The name is absent

10. The name is absent