William Davidson Institute Working Paper 402

equilibrium output declines further on. At some moment in time the decline in output

should be large enough (and unemployment high enough) such that prices start to

decline; the reverse process is at work.

A simple model helps describing the mechanism more precisely. Let the price

equation be a standard Phillips-curve:

dp (t)/ dt

p(t)

= γ[y ( t )- y ]

(1)

where y is the structural output, i.e. the output level associated to the structural

unemployment rate (alternatively, one may carry out this reasoning in output growth

rates instead of levels). Structural unemployment is related to various wage rigidities

and frictions. Notice that in transition economies, this structural rate of unemployment

may be quite high.

Let us denote by R the reserves of foreign exchange of the currency board, by

p* the price level in the EU and by e the official exchange rate. Then, reserves will

follow the dynamic:

dR ( t ) / dt

R ( t )

= α[ep * - p(t)]

(2)

The equilibrium output will respond to the contraction in exports and the money stock

according to:

dy ( t )/ dt _ θ dR ( t )/ dt

y ( t ) R ( t ) ()

Thus equation (2) can be written as:

dy ( t)/dt = αθep *- p (t )] (4)

y(t)

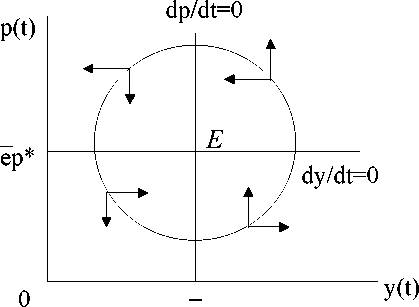

The price level and output motion laws are solutions to the system of

differential equations (1) and (4). One has noticed the similarity between this model

and the famous Predator-prey model. There is a non-trivial stationary point E of

coordinates (y = y, p = ep *). As can be easily observed from the phase diagram

(Figure 1), prices and output display cycles around the equilibrium point. That is,

starting from any other initial point except the stationary point, the price and output

solution belongs to a closed loop (one of the possible paths is depicted in Figure 1,

where the arrows indicate the sense of motion).

y

Figure 1: the Phase diagram

Let us imagine that policymakers have determined the initial exchange rate e

so that the system is stable, that is, it settles at point E. Unfortunately, any exogenous

More intriguing information

1. The name is absent2. Kharaj and land proprietary right in the sixteenth century: An example of law and economics

3. HEDONIC PRICES IN THE MALTING BARLEY MARKET

4. Firm Closure, Financial Losses and the Consequences for an Entrepreneurial Restart

5. Volunteering and the Strategic Value of Ignorance

6. Proceedings of the Fourth International Workshop on Epigenetic Robotics

7. The name is absent

8. The name is absent

9. The name is absent

10. A THEORETICAL FRAMEWORK FOR EVALUATING SOCIAL WELFARE EFFECTS OF NEW AGRICULTURAL TECHNOLOGY