absolute value). Second, the ‘temporary’ changes in the fundamentals and the exogenous

variables may be such that they drive the real exchange rate away from the long run equilibrium

for a prolonged period.

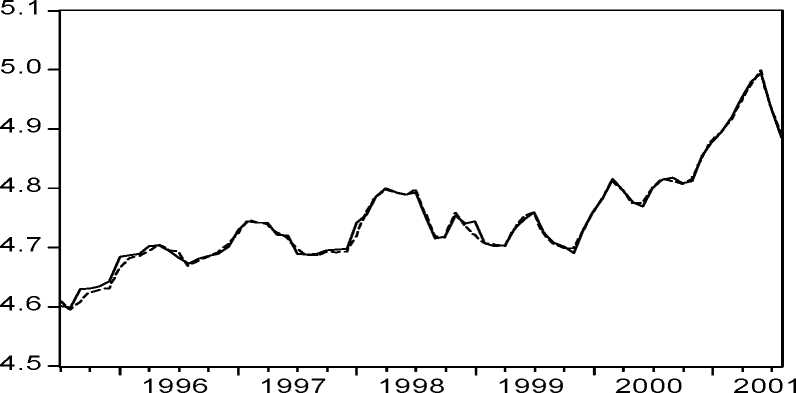

Figures 1, 2, and 3 present the actual real exchange rate and the short run real exchange rate

estimated from the error correction model for Poland and Russia, respectively. They indicate that

the estimated error correction equations capture the movements of the real exchange rates in the

short run very well. 33

--Lnplreer ----lnplreerf

Fig 1. Poland, Actual and Fitted Real Exchange Rates (log), specification 2

* LNPLREER: actual log real exchange rate; LNPLREERF: fitted log real exchange rate

33 Moreover, although not reported here, the within sample forecast error measures (Root Mean Squared Errors,

Mean Absolute Errors, and Mean Absolute Percent Errors) indicate the fitted equations capture the movements of

the observed real exchange rates in the short run.

34

More intriguing information

1. The Role of Land Retirement Programs for Management of Water Resources2. A MARKOVIAN APPROXIMATED SOLUTION TO A PORTFOLIO MANAGEMENT PROBLEM

3. The quick and the dead: when reaction beats intention

4. Road pricing and (re)location decisions households

5. Better policy analysis with better data. Constructing a Social Accounting Matrix from the European System of National Accounts.

6. Sex differences in the structure and stability of children’s playground social networks and their overlap with friendship relations

7. Cyber-pharmacies and emerging concerns on marketing drugs Online

8. Crime as a Social Cost of Poverty and Inequality: A Review Focusing on Developing Countries

9. Restricted Export Flexibility and Risk Management with Options and Futures

10. NATIONAL PERSPECTIVE