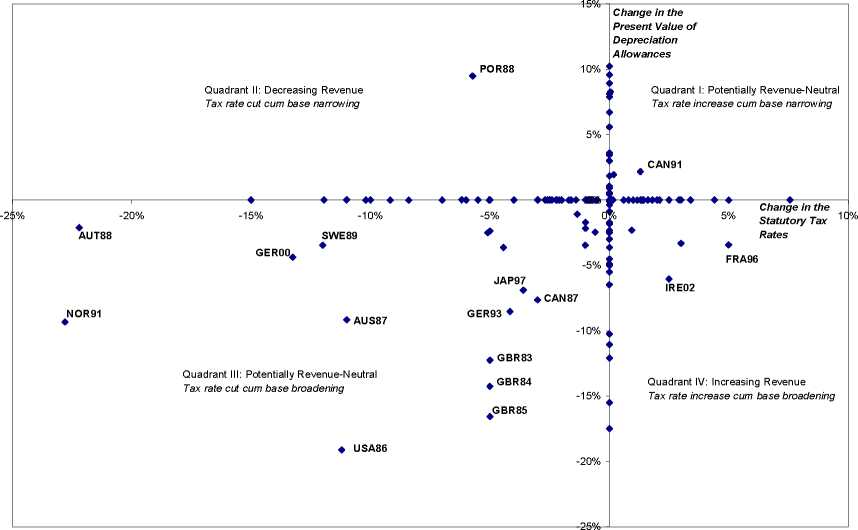

Using the Corporate Tax Data Base provided by the Institute for Fiscal Studies

(IFS) and described and analyzed in Devereux, Griffith & Klemm (2002), diagram

1 depicts each change in the statutory tax rates and the PVDA4 of the OECD

countries enumerated in footnote 1 in the years 1982-2003. The æ-axis measures

changes of the tax rate, the ^-axis the variation in the tax base. Data points which

are not on the axes present a simultaneous change of the tax rate and the tax base.

Thus, we get four quadrants among which two are (potentially) revenue-neutral,

because the variation of one tax parameter is “financed” by the variation of the

other one. In addition, as long as the tax system is on the increasing part of the

Laffer curve, tax reforms in quadrant II are clearly revenue-decreasing and those

in quadrant IV are revenue-increasing.

Diagram 1: Tax reforms in different OECD countries 1982-2003. Data source:

Devereux et al. (2002).

As the diagram shows, a great deal of tax policy reforms consists of a variation

4The change in the PVDA is calculated as an unweighted average of the changes in the PVDA

of plant and machinery and the PVDA of industrial buildings.

More intriguing information

1. AN ECONOMIC EVALUATION OF COTTON AND PEANUT RESEARCH IN SOUTHEASTERN UNITED STATES2. Social Cohesion as a Real-life Phenomenon: Exploring the Validity of the Universalist and Particularist Perspectives

3. Fiscal Policy Rules in Practice

4. The name is absent

5. The name is absent

6. Visual Perception of Humanoid Movement

7. The name is absent

8. The name is absent

9. The Employment Impact of Differences in Dmand and Production

10. The name is absent