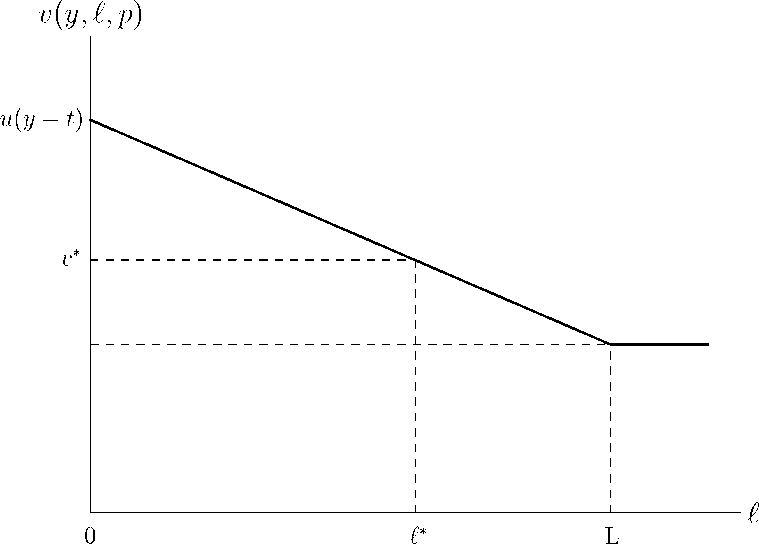

Figure 2: Expected utility as a function of the severity of the illness

Δ = H⅜)>'(y — t) У δ(u)dF(y, €)

— [1+ t'(p)]u'(У — t — P) 2" δ(υ)dF(y,€) (15)

Moreover, (13) can in this case be written as

ʃ δ(υ)dF(y,€) = ʃ δ(υ)dF(y,€) < 0

(16)

since δ(v) > 0 for € > L. The first integral in (15) is in other words negative.

The second integral in (15) is positive, since δ(v~) > 0 for € > L. Since the

terms [—t'(p)] and [1 + t'(p)] are both positive, it follows that Δ < 0 in the

present case. From our previous discussion we thus have the the following

proposition:

10

More intriguing information

1. A Consistent Nonparametric Test for Causality in Quantile2. Campanile Orchestra

3. Housing Market in Malaga: An Application of the Hedonic Methodology

4. The Role of Immigration in Sustaining the Social Security System: A Political Economy Approach

5. Prevalence of exclusive breastfeeding and its determinants in first 6 months of life: A prospective study

6. The name is absent

7. The name is absent

8. Standards behaviours face to innovation of the entrepreneurships of Beira Interior

9. Fighting windmills? EU industrial interests and global climate negotiations

10. The Composition of Government Spending and the Real Exchange Rate