4 ANNEXES

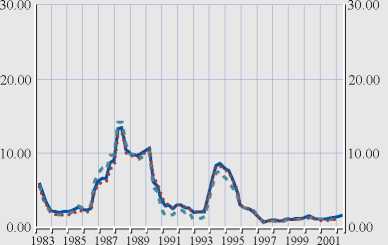

Chart 11 Sectoral shifts and volatility (rescaled) (cont’d)

Denmark

United Kingdom

20.00

0.00

0.00

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

30.00

10.00

20.00

10.00

The figure reports the variance of the aggregate business

cycle component at the actual sectoral specialisation for

each individual observation (solid line) and the variance

of the aggregate business cycle component where the

sectoral specialisation has been fixed at its initial value

(dashed line).

Sources : Eurostat, NCBs, ECB calculations.

Note: See Annex 4.2.2.2 for a discussion of the underlying methodology and a presentation of volatility developments using the same scale for

all countries.

chosen filter parameters, except for agriculture

where very strong reactions can be detected.

4.2.2.2 SECTORAL DECOMPOSITION OF

AGGREGATEVOLATILITY

The decomposition in Table 6 and the

assessment in Chart 9 follow the formula for the

variance of joint distributions:

2 2

Var[ax + by + c] = a Var[x] + b Var[y] + 2abCov[x, y]

In order to facilitate cross-country comparability,

Chart 9 has been reproduced in Chart 11, using

the same scale for all countries.

P к, t = « к + ∑ β, P,, к, t + ε,, к, t

i

where qk,t represents the synchronisation

coefficient of country k at time t and qi,k,t

represents the synchronisation coefficient of

industry i in country k at time t. The regression

coefficients were estimated using the within-

estimator with country-fixed effects, ak, and

accounting for serial correlations of the

synchronisation coefficients as described by

Baltagi and Wu (1999)58. Results were reported

according to whether the bi were found to be

statistically significant at the 5% level or not.

4.2.2.3 SECTORAL DETERMINANTS OF BUSINESS

CYCLE SYNCHRONISATION

The results in Table 11 were established by

running the following regression:

58 B. H. Baltagi and P. X. Wu (1999), “Unequally spaced panel data

regressions with AR(1) disturbances”, Econometric theory, 15,

pp. 814-823.

ECB

Occasional Paper No. 19

July 2004

More intriguing information

1. Eigentumsrechtliche Dezentralisierung und institutioneller Wettbewerb2. Developmental Robots - A New Paradigm

3. Non-causality in Bivariate Binary Panel Data

4. Barriers and Limitations in the Development of Industrial Innovation in the Region

5. The name is absent

6. The name is absent

7. The problem of anglophone squint

8. The name is absent

9. The Role of Immigration in Sustaining the Social Security System: A Political Economy Approach

10. The name is absent