-18-

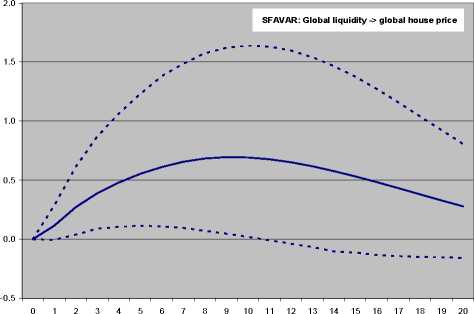

study conducted by Alessi, Detken (2009) finds that global measures of liquidity, like the

M1 gap and the private credit gap, are useful early warning indicators for aggregate asset

price booms in OECD countries. Their asset price measure includes house prices as well

as commercial property and share prices.

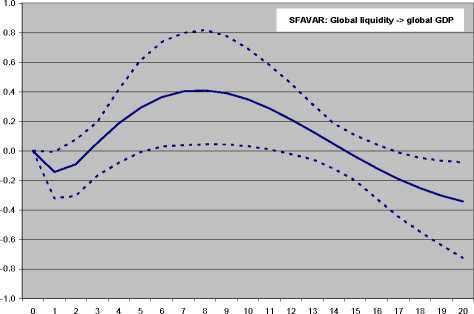

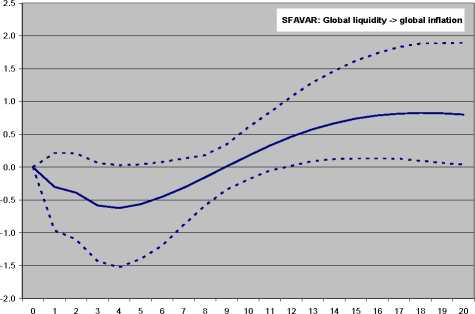

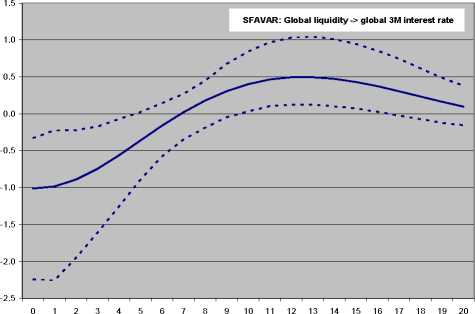

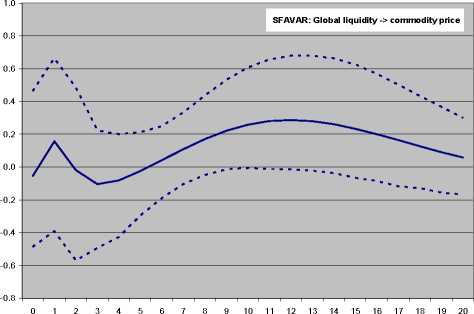

Chart 1 - Impulse response analysis in SFAVAR (global liquidity shock)

More intriguing information

1. Structural Breakpoints in Volatility in International Markets2. The name is absent

3. Transport system as an element of sustainable economic growth in the tourist region

4. Bird’s Eye View to Indonesian Mass Conflict Revisiting the Fact of Self-Organized Criticality

5. Imitation in location choice

6. LOCAL CONTROL AND IMPROVEMENT OF COMMUNITY SERVICE

7. The name is absent

8. Political Rents, Promotion Incentives, and Support for a Non-Democratic Regime

9. Real Exchange Rate Misalignment: Prelude to Crisis?

10. If our brains were simple, we would be too simple to understand them.