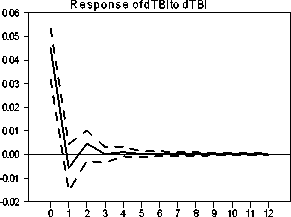

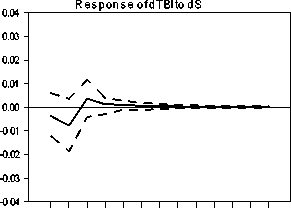

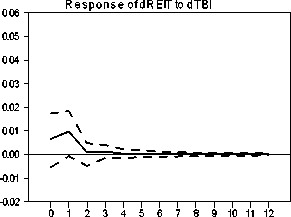

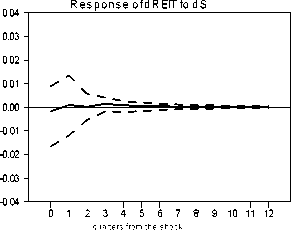

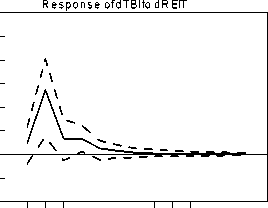

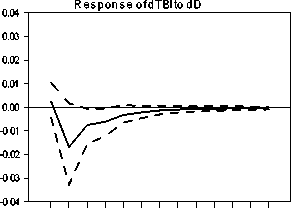

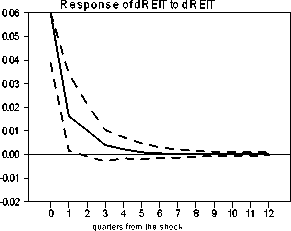

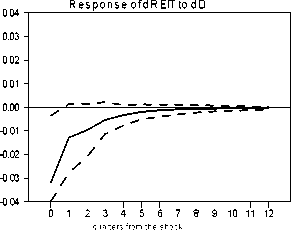

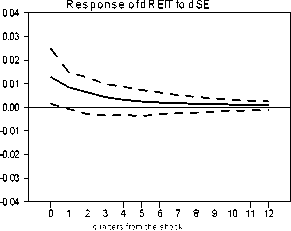

Figure 3 The reactions of the securitized and direct industrial property returns to shocks in the fundamentals

quarters from the shock

01 23456789 10 11 12

quarters from the shock

quarters from the shock

0.06

0.05

0.04

0.03

0.02

0.01

0.00

-0.01

-0.02

01 23456789 10 11 12

quarters from the shock

0123456789 10 11 12

quarters from the shock

-0.04

Response of dTBI to dIRN

0.04

0.00

0.03

0.02

0.01

-0.01

-0.02

-0.03

0123456789 10 11 12

-0.04

Response ofdTBIto dSE

0.04

0.00

0.03

0.02

0.01

-0.01

-0.02

-0.03

01 23456789 10 11 12

quarters from the shock

quarters from the shock

Response of dRET to dIRN

0.04 -∣---------------------------------------------------------------------

0.03 - ∖

0.02 -

4

0.01 - X

____ X

0.00-- ʌ-Z~Z∑3 = ≈""∣

-0.01 - " *"

-0.02 -

-0.03 -

-0.04 --------------1-----------1------------1-----------1-----------1-----------1------------1-----------1-----------1------------1-----------1-----------1------------1-

01 23456789 10 11 12

quarters from the shock

22

More intriguing information

1. CAN CREDIT DEFAULT SWAPS PREDICT FINANCIAL CRISES? EMPIRICAL STUDY ON EMERGING MARKETS2. Draft of paper published in:

3. The name is absent

4. School Effectiveness in Developing Countries - A Summary of the Research Evidence

5. Dynamic Explanations of Industry Structure and Performance

6. Towards Learning Affective Body Gesture

7. DIVERSITY OF RURAL PLACES - TEXAS

8. The Role of Evidence in Establishing Trust in Repositories

9. DURABLE CONSUMPTION AS A STATUS GOOD: A STUDY OF NEOCLASSICAL CASES

10. A parametric approach to the estimation of cointegration vectors in panel data