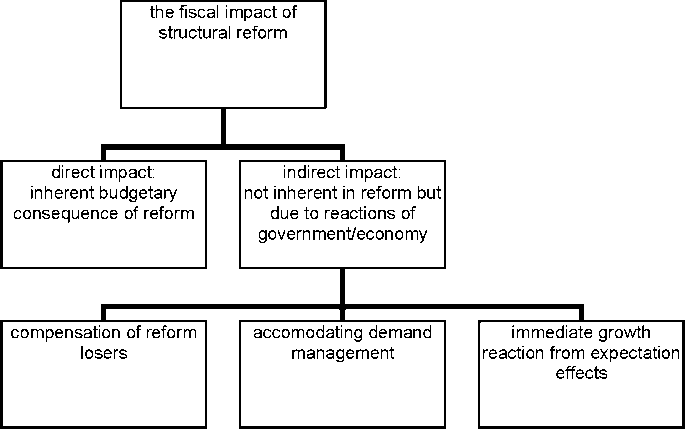

Classification of fiscal effects

In the context of a macroeconomic analysis based on a country panel it is hardly possible to

precisely differentiate between the different “stories” being told about the evolution of budgetary

policy over a reform cycle (as summarized in figure 1). However, the following properties of

reform cycles may offer insights:

While a deterioration of the cyclically adjusted deficit in the course of reforms may be related to

either the direct reform consequences, to demand management considerations or to the

compensation aspect, a more detailed look at specific categories of the budget may be helpful to

differentiate: If, for example, an increase in social spending were behind the deficit deterioration

this could be regarded to back the compensation story. Conversely, a largely unspecific increase

in the deficit during reform processes tends to support rather the demand management view.

Furthermore, if reforms touch the budget mainly via business cycle effects this should be

detectable from cyclical variables such as growth, output gap or - more directly and scrutinized

explicitly in the following empirical steps - from sentiment indicators.

Figure 1: Classification of budgetary effects of structural reforms

137

More intriguing information

1. Delayed Manifestation of T ransurethral Syndrome as a Complication of T ransurethral Prostatic Resection2. A Review of Kuhnian and Lakatosian “Explanations” in Economics

3. Short Term Memory May Be the Depletion of the Readily Releasable Pool of Presynaptic Neurotransmitter Vesicles

4. The Mathematical Components of Engineering

5. Towards a Mirror System for the Development of Socially-Mediated Skills

6. Spousal Labor Market Effects from Government Health Insurance: Evidence from a Veterans Affairs Expansion

7. The name is absent

8. Ability grouping in the secondary school: attitudes of teachers of practically based subjects

9. Macro-regional evaluation of the Structural Funds using the HERMIN modelling framework

10. sycnoιogιcaι spaces