114

M. Tirelli

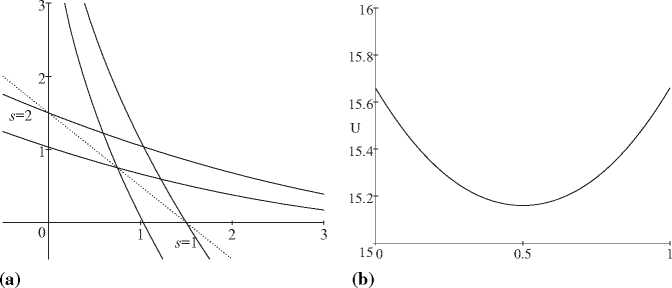

equilibrium). In Fig. 2(b) below, we plot the aggregate (indirect) utility level

as a function of the return from holding the firm in state 1 (i.e., θ1y1), and

fixed x0, when allocations are feasible in the sense of Diamond. It is im-

mediate that the minimum welfare is obtained at the symmetric allocation,

while the only two CPO are corner solutions. Thus, Fig. 2(b) shows that

at a minimum welfare point, the symmetric equilibrium is a local CPO-

equilibrium: a Pareto superior equilibrium can be achieved by a Diamond

central planner via discrete portfolios and production reallocations.

- Optimal tax reforms 1. (Interior equilibrium) We start from the interior

equilibrium, and assume that a tax reform, such as the one considered in

Example 1, is introduced: dt1 = (-1, -5) %. Then a Pareto improvement

is obtained with a .04% increase in the utility of both agents, and an 4.17%

increase in the share of agent 1 in the firm:

|

% Ax 0 |

% Ax ] |

% Ax 2 |

% Aθ |

% Au | |

|

h=1 |

-7.86 |

1. 06 |

1.98 |

4.17 |

.04 |

|

h=2 |

7.86 |

-1. 06 |

-1.98 |

-4.17 |

.04 |

2. (Corner equilibria) Since the two corner equilibria are symmetric, we

consider only the one in which consumer 1 is the single owner of the firm.

The tax reform dt1 = (.1, 0) % is weakly Pareto improving:

|

% Ax 0 |

% Ax ] |

% Ax 2 |

% Aθ |

% Au | |

|

h=1 |

-.05 |

0.5 |

0 |

0 |

.06 |

|

h=2 |

0.5 |

-0.5 |

0 |

0 |

0 |

In words, a (global) CPO equilibrium can be improved upon by using pro-

portional income taxes.

Fig. 2.

More intriguing information

1. TINKERING WITH VALUATION ESTIMATES: IS THERE A FUTURE FOR WILLINGNESS TO ACCEPT MEASURES?2. Poverty transition through targeted programme: the case of Bangladesh Poultry Model

3. Estimated Open Economy New Keynesian Phillips Curves for the G7

4. A MARKOVIAN APPROXIMATED SOLUTION TO A PORTFOLIO MANAGEMENT PROBLEM

5. IMPROVING THE UNIVERSITY'S PERFORMANCE IN PUBLIC POLICY EDUCATION

6. Housing Market in Malaga: An Application of the Hedonic Methodology

7. What should educational research do, and how should it do it? A response to “Will a clinical approach make educational research more relevant to practice” by Jacquelien Bulterman-Bos

8. HEDONIC PRICES IN THE MALTING BARLEY MARKET

9. The name is absent

10. Who’s afraid of critical race theory in education? a reply to Mike Cole’s ‘The color-line and the class struggle’