•4

Review of Islamic Economics, Vol. 8, No. 2, 2004

estimated the function with the associated input share equations,

derived using the Shephard’s Lemma, 11 But the difficulty is that their

derivation implies that the PUs are using their long run efficient input

mix, i.e. the firms are assumed allocatively efficient. Hence, most

studies now estimate a single cost function. This is possible because

many PUs, in fact, produce a single output, and others can aggregate

their multiple outputs into a single output index (Kebede, 2001: 13).

In a simple single output and multiple inputs case, we estimate

the frontier using the functional relationships:

(ɪ)

clt=f(y,v wkt> + ¾

where εit = Vjt+Ujt

In (2) Cll is the total cost of PUi in a period t, y-t and ιι>kt are

vectors of output and input prices respectively f (yll ; w∣,t) provides the

cost frontier. The random disturbance term εjt allows the function to

vary stochastically. It has two components: the υ∙ts are independently

and identically distributed (Hd) elements; they are truly uncorrelated

with the regression. In contrast, the ujls are non-negative variations

associated with the technical inefficiency of the PUi. Thus, the error

term e is not symmetric as u∣t ≥ o.'i

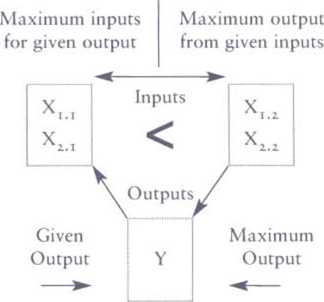

Figure 2: Results Need not be Identical

Estimating the PU-Specific inefficiency is the ultimate objective of

the model. This requires the extraction of separate estimates for and

More intriguing information

1. HEDONIC PRICES IN THE MALTING BARLEY MARKET2. A Location Game On Disjoint Circles

3. The name is absent

4. Qualification-Mismatch and Long-Term Unemployment in a Growth-Matching Model

5. The Structure Performance Hypothesis and The Efficient Structure Performance Hypothesis-Revisited: The Case of Agribusiness Commodity and Food Products Truck Carriers in the South

6. Tariff Escalation and Invasive Species Risk

7. The name is absent

8. WP 48 - Population ageing in the Netherlands: Demographic and financial arguments for a balanced approach

9. Changing spatial planning systems and the role of the regional government level; Comparing the Netherlands, Flanders and England

10. FASTER TRAINING IN NONLINEAR ICA USING MISEP