Current Agriculture, Food & Resource Issues

D. Sparling and E. van Duren

3. acquisitions of divested Canadian business units or facilities of companies,

which may or may not be owned by Canadian firms. Divestitures are

differentiated by the fact that the entire company is not purchased.

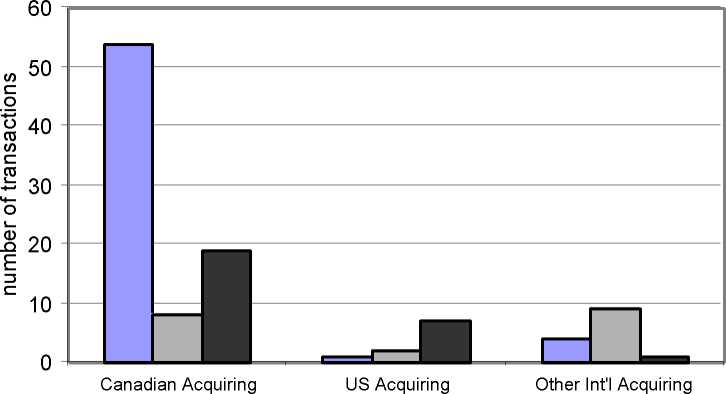

In figure 8, one can see that over the period, Canadian firms acquired predominantly

private companies. U.S. firms tended to purchase divested business units of Canadian

companies, and other international firms showed a preference for Canadian public

companies.

In terms of transaction value, only 76 of 174 transactions reported the value. Reported

value distribution did not show any particular pattern for the five-year period. The

distribution of value over the entire period is shown in figure 9. For those transactions,

cash was definitely the preferred payment option, although 2000 showed a flurry of mixed

deals (figure 10).

Spin-offs are occurring as well.

One of the interesting misconceptions is that mergers and acquisitions are a one-way

street. This is definitely not true. In the United States, in the ten-year period prior to 1998

an average of 50 new companies per year, or roughly 10 percent of IPOs, were carve-outs

from large companies.2 Spin-offs are even more common. In the first nine months of

1998, 300 spin-offs were launched on the U.S. stock market. Many more business units

move between companies. In Canada, for example, Maple Leaf Foods made one bakery

□ Canadian Private □ Canadian Public □ Canadian Divestiture

Figure 8 Nature of the acquired Canadian company or business unit, 1996-2000

Source: Annual Directory of Mergers and Acquisitions in Canada, 1996-2000

40

More intriguing information

1. The name is absent2. Convergence in TFP among Italian Regions - Panel Unit Roots with Heterogeneity and Cross Sectional Dependence

3. The Nobel Memorial Prize for Robert F. Engle

4. DETERMINANTS OF FOOD AWAY FROM HOME AMONG AFRICAN-AMERICANS

5. Educational Inequalities Among School Leavers in Ireland 1979-1994

6. Improving the Impact of Market Reform on Agricultural Productivity in Africa: How Institutional Design Makes a Difference

7. The Impact of Minimum Wages on Wage Inequality and Employment in the Formal and Informal Sector in Costa Rica

8. Strengthening civil society from the outside? Donor driven consultation and participation processes in Poverty Reduction Strategies (PRSP): the Bolivian case

9. ENVIRONMENTAL POLICY: THE LEGISLATIVE AND REGULATORY AGENDA

10. The name is absent