Current Agriculture, Food & Resource Issues

D. Sparling and E. van Duren

Industry

Convergence Geographic Roll-

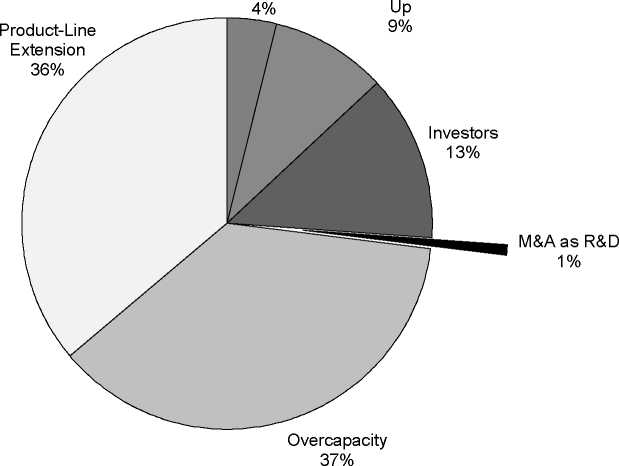

Figure 2 Rationales for merger and acquisition activity, 1997-1999

These data are from all U.S. M&A deals between 1997 and 1999 over U.S. $ 500

million, where acquiring and acquired companies or divisions could be identified by four-

digit SIC code. In total, 1036 deals were analyzed.

Source: Bower, J.L. 2001. Not all M&A are Alike and That Matters. Harvard Business Review

March: 92-101

meets targets, thus forcing managers to continually search for acquisitions to satisfy

market expectations. Financial markets and managers also tend to operate in cycles. When

cash is readily available M&A activities increase dramatically, a trend obvious in 1999

and early 2000. High stock prices fuel this activity, as firms pay for acquisitions with

overvalued stock. Frequently, the first big mergers in an industry will accelerate the pace

of merger activity, as companies scramble to keep pace with competitors. Mergers and

acquisitions become part of the market psyche (Ghemawat and Ghadar, 2000).

Key Drivers in Large U.S. Mergers and Acquisitions

Bower (2001) examined U.S. mergers and acquisitions over $500 million in value

during the period 1997-1999. The analysis revealed that for these large transactions,

overcapacity and product-line extension were the major reasons for the deals, but

convergence, R&D and investor motivation were also factors (figure 2). If smaller deals

were examined, the distribution of motivation would change, with almost certainly more

emphasis on R&D. Few R&D mergers reach the $500 million value level.

34

More intriguing information

1. The Impact of EU Accession in Romania: An Analysis of Regional Development Policy Effects by a Multiregional I-O Model2. EMU's Decentralized System of Fiscal Policy

3. Public-Private Partnerships in Urban Development in the United States

4. Multimedia as a Cognitive Tool

5. The name is absent

6. Conflict and Uncertainty: A Dynamic Approach

7. The name is absent

8. The name is absent

9. MICROWORLDS BASED ON LINEAR EQUATION SYSTEMS: A NEW APPROACH TO COMPLEX PROBLEM SOLVING AND EXPERIMENTAL RESULTS

10. Evaluation of the Development Potential of Russian Cities