Ludwig Theuvsen and Christoph Niederhut-Bollmann 355

ved very differently by the respondents. In the opinion of larger breweries, tThe situation is

considered more critical by larger breweries since these companies rely more heavily on mar-

keting channels, such as retailers, in which the competitive pressures stemming from substitute

products are highest.

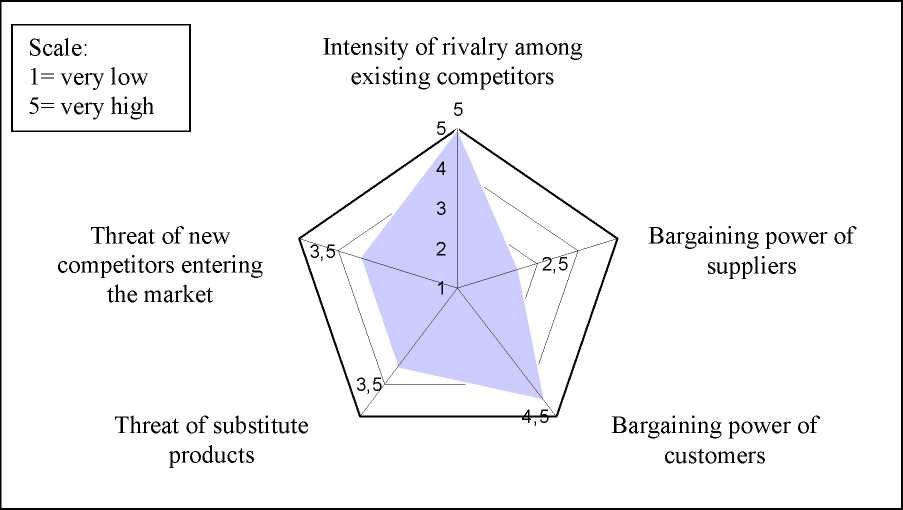

Figure 1 summarizes the perceived market risks of among the surveyed breweries surveyed.

Disregarding size-dependent differences, it displays the mean value of for all respondents. Ri-

valry among existing competitors and the bargaining power of retailers are considered the most

important market risks. Ranked next are the threat of substitutes and new competitors. The risk

stemming from the bargaining power of suppliers is seen as least important. All in all, breweries

of different sizes perceive these market risks quite differently. We hypothesize that this reveals

different strategies and the different risks associated with these strategies. Therefore, strategic

risk management in the German brewing industry is analyzed in more detail in the following-

below. We start with risk management strategies on the corporate level and then proceed with

the contribution of competitive strategies to risk management.

Figure 1. Perceived Market Risks in the German Brewing Industry

4 Strategic Risik Management in the German Brewing Industry

Between 1995 and 2004, the total number of breweries in Germany has remained nearly con-

stant. Nevertheless, a closer look at Table 2 reveals that this is only due only to the growing

number of micro-breweries;, whereas the number of breweries with an annual output between

5,000 and one million hectoliters has beenactually declinedshrinking rapidly. So, obviously,

deisinvestmenting and leaving the industry has turned out to becomewere a common strategiesy

tofor avoiding risks in an more and moreincreasingly competitive industry.

More intriguing information

1. Olive Tree Farming in Jaen: Situation With the New Cap and Comparison With the Province Income Per Capita.2. Ongoing Emergence: A Core Concept in Epigenetic Robotics

3. The name is absent

4. The name is absent

5. Are combination forecasts of S&P 500 volatility statistically superior?

6. The Folklore of Sorting Algorithms

7. The name is absent

8. Orientation discrimination in WS 2

9. Heterogeneity of Investors and Asset Pricing in a Risk-Value World

10. Auction Design without Commitment