This modification and extension of the baseline disequilibrium AS-AD model of Asada,

Chen, Chiarella and Flaschel (2004) in particular goes beyond this earlier approach as

it now also allows for positive effects of real wage changes on aggregate demand, not yet

present in the AD component of our original modification of the conventional AS-AD

dynamics.

The above model - though not microfounded by making the representative household

assumption - is microfounded in the way Keynesian theory was microfounded after

Patinkin and it also makes use of recent approaches, to labor market dynamics as in

Blanchard and Katz (2000). With respect to empirically relevant restructuring of the

theoretical framework it is as pragmatic as for example the approach employed by Rude-

busch and Svensson (1999). By and large we therefore believe that it represents a working

alternative to the New Keynesian approach, in particular when the critique of the latter

approach is taken into account. It overcomes the weaknesses and the logical inconsisten-

cies of the Neoclassical synthesis, stage I, and it does so in a minimal way from a mature

traditional Keynesian perspective (that is not really ’New’). It preserves the problematic

nature of the real rate of interest channel, where the stabilizing Keynes effect (or the in-

terest rate policy of the central bank) is interacting with the destabilizing, expectations

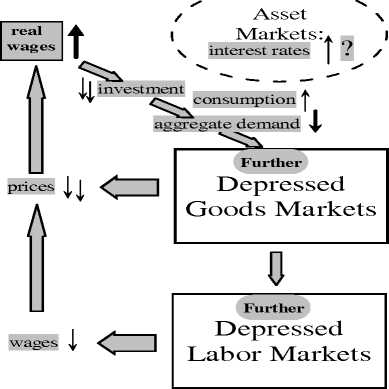

driven Mundell effect. And it preserves the real wage effect of the Neoclassical synthesis,

stage I, where - due to a negative dependence of aggregate demand on the real wage

- we have that price flexibility is destabilizing, while wage flexibility is not. This real

wage channel is not a topic in the New Keynesian approach, due to the specific form of

wage-price dynamics there considered, see for example Woodford (2003, p.225), and it is

summarized in the figure 1 for the situation where investment dominates consumption

with respect to real wage changes. In the opposite case, the situations considered will

be reversed with respect to their stability implications.

Normal Rose Effect (example):

real

wages

Asset

Markets:

interest rates

investment

I ^^ʌænsumption

aggregate demand

prices ∣

Recovery!

Depressed

Goods Markets

wages

-ɔ Recovery!

Depressed

Labor Markets

Adverse Rose Effect (example):

Figure 1: Rose effects: The real wage channel of Keynesian macrodynamics .

The feedback channels just discussed will be the focus of interest in the now following

More intriguing information

1. Palkkaneuvottelut ja työmarkkinat Pohjoismaissa ja Euroopassa2. The name is absent

3. The name is absent

4. The name is absent

5. The name is absent

6. GROWTH, UNEMPLOYMENT AND THE WAGE SETTING PROCESS.

7. Julkinen T&K-rahoitus ja sen vaikutus yrityksiin - Analyysi metalli- ja elektroniikkateollisuudesta

8. Secondary school teachers’ attitudes towards and beliefs about ability grouping

9. Apprenticeships in the UK: from the industrial-relation via market-led and social inclusion models

10. Feeling Good about Giving: The Benefits (and Costs) of Self-Interested Charitable Behavior