Spectral calibration of exponential Levy models ??

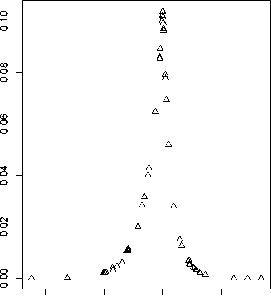

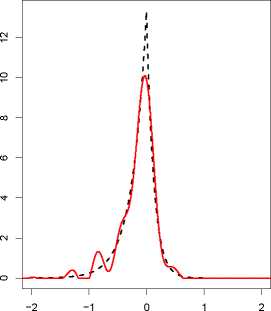

-2 -1 0 1

log-moneyness x

(Oj ) as function of xj .

Fig. 1. Kou model. Left: Simulated option price data

Right: Calibrated Levy density ^ and true ν (dashed).

Both methods have certain distinctive features. In the PLS method the

penalisation plays a double role, it uses prior knowledge for the unknown

Levy triplet and it stabilizes the inverse problem. Because of the relative

entropy penalisation, the volatility σ is fixed in advance by the prior and

cannot be calibrated. In comparison, the spectral calibration (SC) method

profits from the regularity of the jump density for regularizing the inverse

problem. In particular, the volatility can be calibrated. The SC estimators

depend only on one critical tuning parameter, the cut-off frequency U , and

given U they are always uniquely defined.

In simulations the experience is that both methods yield roughly com-

parable results. The PLS method fits better the option price function, while

the SC method performs better in estimating the Levy triplet. The PLS

method has difficulties in estimating the jump density near zero, because

there are no smoothness constraints, while the SC method can yield nega-

tive values for jump densities, which should be corrected a posteriori, see

Belomestny and Reiβ (2006). Because it avoids a numerical minimisation

procedure, the SC method is considerably faster than the PLS method.

3.3. A numerical example

We consider the double exponential jump diffusion model proposed by Kou

(2002), where the Levy triplet is specified by the jump density

ν(x) = λ(pλ + e-λ + x 1[o∞)(x) + (1 -p)λ-eλ-x 1(-∞,ɑ)(x)´, x ∈ R, (20)

and the parameters σ, λ, λ+, λ- > 0 and p ∈ [0, 1], while γ is uniquely

determined by the martingale condition. We simulate the Kou model with

More intriguing information

1. The name is absent2. New issues in Indian macro policy.

3. Survey of Literature on Covered and Uncovered Interest Parities

4. The name is absent

5. DISCRIMINATORY APPROACH TO AUDITORY STIMULI IN GUINEA FOWL (NUMIDA MELEAGRIS) AFTER HYPERSTRIATAL∕HIPPOCAMP- AL BRAIN DAMAGE

6. The name is absent

7. WP 36 - Women's Preferences or Delineated Policies? The development or part-time work in the Netherlands, Germany and the United Kingdom

8. El impacto espacial de las economías de aglomeración y su efecto sobre la estructura urbana.El caso de la industria en Barcelona, 1986-1996

9. Alzheimer’s Disease and Herpes Simplex Encephalitis

10. THE CO-EVOLUTION OF MATTER AND CONSCIOUSNESS1