Journal of Applied Economic Sciences

Volume IV/ Issue 1(7)/ Spring 2009

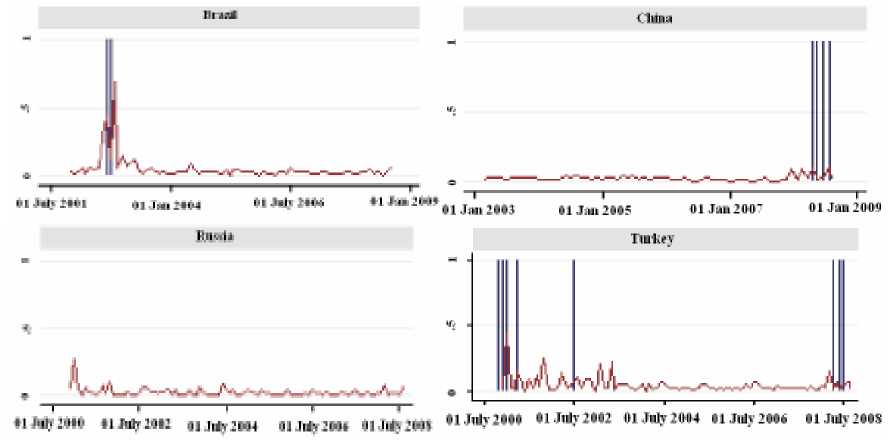

Looking at country-specific forecasts, the most successful prediction of a stock market crisis

was for the Brazilian Bovespa index. Also, the model produced successful predictions for the Turkish

stock market with the exception of predicted values for 2003. The worst results from the stock market

model are for the Russian stock market index where we have a predicted crisis probability of more

than 20 percent and yet there is no crisis as defined in this paper. Figure 1 below shows four graphs of

interest for forecasts for stock market crises by country.

Figure 1. Graphs’ of model (2) forecasts for stock market crises for four countries. The blue bar shows the

occurrence of a crisis as defined in this paper and the red line shows the estimated probability of a crisis by

model(2)

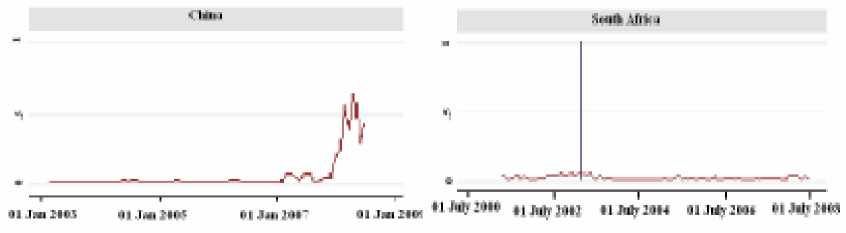

On the other hand, the most successful prediction of a currency market crisis was for the South

African Rand in 2003, although we don’t have a predicted crisis probability of more than 10 percent

for this currency. The worst result from the model that predicts currency crises was for the Chinese

Renminbi. The model predicts a currency crash with more than 50 percent probability during the

second quarter of 2008 although there is no crisis. Figure 2 below shows the graphs of forecasts for

currency market crises by country.

Figure 2. Graphs’ of model (2) forecasts for currency market crises for two currencies.

The blue bar shows the occurrence of a crisis as defined in this paper and the red line shows the estimated

probability of a crisis by model(2)

To sum up, changes in sovereign credit default swap premiums have statistically significant

impact on the probability of stock market crises in emerging markets, while the same is not true for

the currency crises. Credit default swaps alone were able to predict 40% of the stock market crises

and 4.76% of the currency market crises.

135

More intriguing information

1. THE INTERNATIONAL OUTLOOK FOR U.S. TOBACCO2. SAEA EDITOR'S REPORT, FEBRUARY 1988

3. Social Irresponsibility in Management

4. The Composition of Government Spending and the Real Exchange Rate

5. The Economics of Uncovered Interest Parity Condition for Emerging Markets: A Survey

6. Eigentumsrechtliche Dezentralisierung und institutioneller Wettbewerb

7. Density Estimation and Combination under Model Ambiguity

8. ADJUSTMENT TO GLOBALISATION: A STUDY OF THE FOOTWEAR INDUSTRY IN EUROPE

9. CGE modelling of the resources boom in Indonesia and Australia using TERM

10. The name is absent