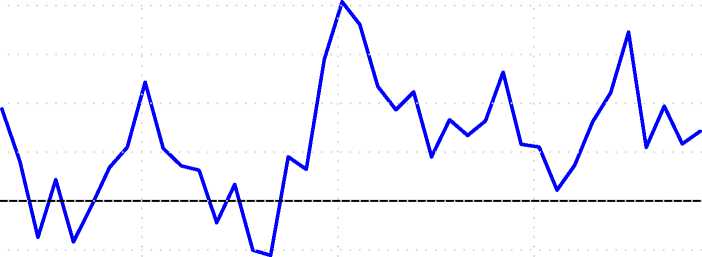

Figure 6 Net profit growth of non-financial firms (year-on-year)

2000

2005

trillion. With roughly 31% of gross tax revenues coming from this source, volatility in

corporation tax revenues is now an important influence on the overall fiscal situation.

Figure 6 shows the net profit growth, on a year-on-year basis, of all non-financial firms

observed in the CMIE database. These firms account for the bulk of corporation

tax payments to the government. This graph shows that we have experienced a

remarkable 21-quarter period of high and sustained net profit growth. However, net

profit growth of corporations even turns negative in a business cycle downturn - as

seen in September 1998 to September 1999, and from March 2001 to March 2002.

Thus, in a future business cycle downturn, corporation tax growth will not be buoy-

ant, and the nominal tax collections in a particular year could even decline when

compared with the previous year. In a future business cycle downturn, income tax

is also likely to suffer poor growth. The two key elements which have powered the

improvement in the fiscal situation are, hence, elements which have a fairly high

exposure to business cycle conditions. With the high reliance on income tax, the

volatility of tax revenues is now higher than it used to be.

• Expenditures on welfare programs Table 4 shows that central gross tax revenue im-

proved by 3.6 percentage points from 1998-99 to 2006-07. Roughly speaking, 30%

of central gross tax revenue is sent to the states, so the additional resources to the

centre were roughly 2.5 percent of GDP. Expenditure compression yielded another

0.4 percent of GDP, adding up to a reduction in the central gross fiscal deficit of 2.9

percent of GDP. The bulk of the contribution to fiscal consolidation has, thus, come

from improved tax collections (2.5 percent of GDP) rather than from expenditure

reductions (0.4 percent of GDP). This is in contrast with the international experi-

ence with successful fiscal consolidations, where a drop in current expenditure plays

17

More intriguing information

1. Workforce or Workfare?2. The name is absent

3. The open method of co-ordination: Some remarks regarding old-age security within an enlarged European Union

4. Kharaj and land proprietary right in the sixteenth century: An example of law and economics

5. The name is absent

6. The Values and Character Dispositions of 14-16 Year Olds in the Hodge Hill Constituency

7. The name is absent

8. Analyzing the Agricultural Trade Impacts of the Canada-Chile Free Trade Agreement

9. The name is absent

10. Migrant Business Networks and FDI