changes in a monetary union arise from preference aggregation. Here, structural policy

changes are important and therefore only structural differences across economies are

allowed. This, of course, abstracts from many effects that have been discussed in the

literature, focusing on differences in preferences in the creation of fixed exchange rates and

monetary unions (see e.g. Berger et al. 2001).

2.2. The Situation before Monetary Union

As a benchmark, I begin with the situation before monetary union where countries have

monetary autonomy. Assuming that exchange rates follow purchasing power parity ensures

that exchange rate movements have no influence on output, and that the rate of inflation is

determined by domestic monetary policy only.

The game structure used is Stackelberg where the fiscal authority is the Stackelberg

leader; the solution concept is subgame-perfect equilibrium. The time structure is as

follows: (i) the government decides about the structural reform package si implying a

certain fiscal policy package xi , (ii) having observed this, the private sector forms

expectations about the rate of inflation πie, (iii) the central bank sets the rate of inflation πi ,

and (iv) output is determined. The model is solved by backward induction.

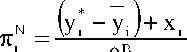

Since the government is Stackelberg leader it takes the reaction of the central bank

into account when making its policy choices. The central bank's best response is

N

πi

πe + (y* - Yi )+ xi

1 + θB

(5)

which, with rational expectations, becomes

(6)

More intriguing information

1. The Functions of Postpartum Depression2. Testing Hypotheses in an I(2) Model with Applications to the Persistent Long Swings in the Dmk/$ Rate

3. Prizes and Patents: Using Market Signals to Provide Incentives for Innovations

4. The name is absent

5. Une Classe de Concepts

6. The name is absent

7. Migration and employment status during the turbulent nineties in Sweden

8. The Complexity Era in Economics

9. The name is absent

10. Towards Teaching a Robot to Count Objects