Wiemer Salverda

Source: 1977-1999 own calculations based on IPO data and 2001-2003 Statline (level adapted by 1999 ratios) and CPB, MEV2006

Table A.7 and CBS population statistics.

Direct income data from the Income panel survey (IPO) of Statistics Netherlands can address these

problems. While the AOW goes exclusively to people aged 65 and over, occupational pensions and

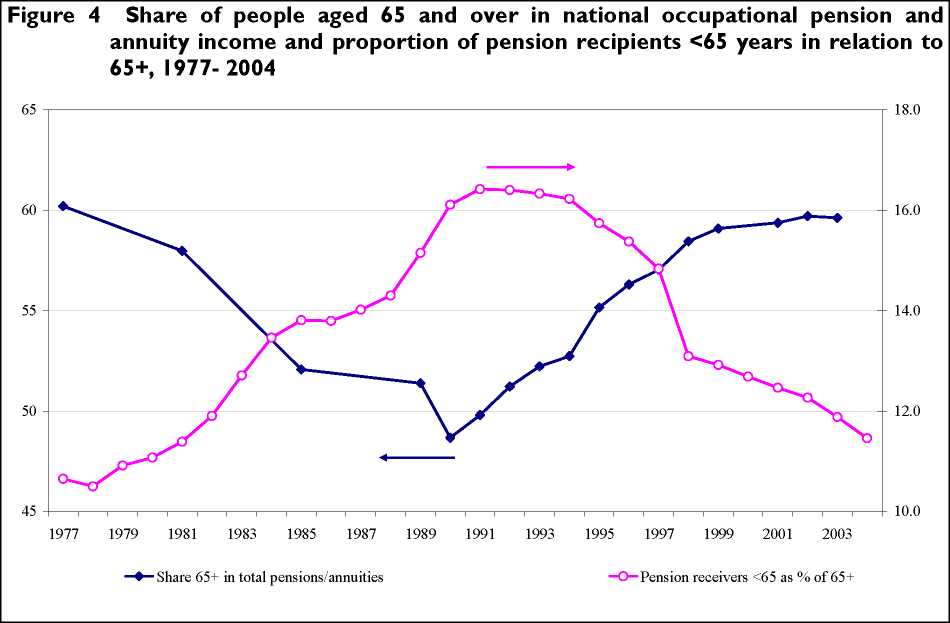

annuities do not. Figure 4 shows the share of the aged in the national total of pension and annuity

receipts according to the IPO. The figure dropped to a low of 47% in 1990, only to climb back to its

original level of 60% now. This picture is consistent with the fluctuation from 10.5 up to 16.5% and

down again to 11.5% in the numbers in early retirement relative to the persons aged 65 and over

which is also shown in Figure 42. Finally, the contribution of other forms of income for older people

(from enterprise or work, interest, dividends and benefits such as rent subsidies, child allowances

and social security) is not insignificant, despite having fallen considerably from 18 to 11% (not

shown).

The IPO data also offer direct insights into the financial OADR - that is, the ratio of total relevant

incomes of those aged 65+ to the total relevant incomes of those aged 20-64. This can again be

defined on a calendar and a cohort basis. Occupational pensions and life-insurance payments are

made on the basis of savings out of older people’s previous personal contributions and therefore

relate to the cohort-OADR. Figure 5 shows the financial calendar-OADR and the corresponding

demographic OADR, both calendar-based. After a decrease, the former fluctuates at around 11%,

2 Total number of people with early or survivor’s pension taken as a percentage of the population aged 55 to 64 years.

18

AIAS - UvA

More intriguing information

1. What Drives the Productive Efficiency of a Firm?: The Importance of Industry, Location, R&D, and Size2. Indirect Effects of Pesticide Regulation and the Food Quality Protection Act

3. Tobacco and Alcohol: Complements or Substitutes? - A Statistical Guinea Pig Approach

4. The name is absent

5. Optimal Taxation of Capital Income in Models with Endogenous Fertility

6. The name is absent

7. An Efficient Secure Multimodal Biometric Fusion Using Palmprint and Face Image

8. Pass-through of external shocks along the pricing chain: A panel estimation approach for the euro area

9. Legal Minimum Wages and the Wages of Formal and Informal Sector Workers in Costa Rica

10. The name is absent