Population ageing in the Netherlands: Demographic and Financial arguments for a balanced approach

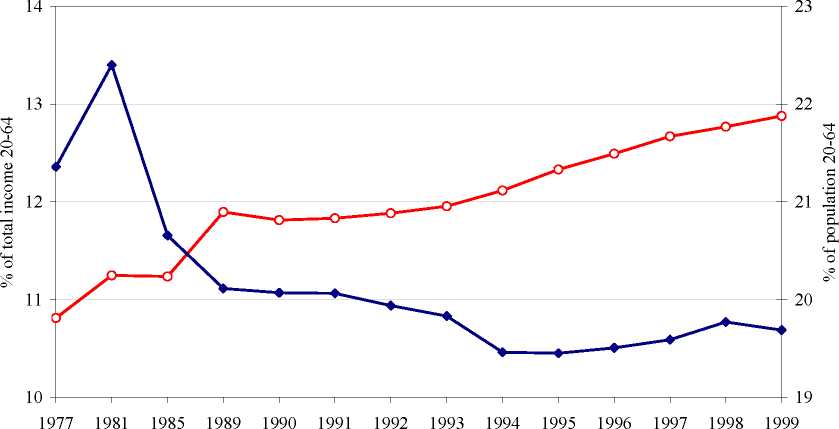

while the latter rises slowly to 23%. The number of older income earners rises but because their

average income lags behind at the same time, there is only a small change in the aggregate ratio. The

outcome contradicts that older people would have become richer in relative terms.

Figure 5 Financial OADR* (left axis) and demographic OADR (right axis), 1977-1999

Dem Demo graphic ♦ Financial

*) AOW received by 65+ as % of total income of 20-64-year-olds; those who received the AOW abroad are

not included, in contrast to Figure 3.

Source: own calculations from CBS, income panel survey (Atkinson and Salverda, 2005, explain the nature of the data).

The IPO data can also provide insight into the different income components. At approximately 55%,

the contribution of the AOW to total 65+ income is significantly larger than the 40% calculated

above on a GDP basis - in actual fact, the difference is even greater because income components

other than pensions are included here in total income as well. The AOW contribution is no longer

falling but remains almost unchanged. Although occupational pensions and annuities once again make

up a growing share, their significance in quantitative terms is considerably less - one third, as against

60% calculated on a GDP basis. Strikingly enough, occupational pensions and AOW together do not

amount to 70% of previous earnings, something which is confirmed by data provided to the author

by ABP and PGCM, the two largest pension funds in the Netherlands (and very large by

international standards as well). In 2004, newly retired people had an average pension accrual of 25

AIAS - UvA

19

More intriguing information

1. A Rational Analysis of Alternating Search and Reflection Strategies in Problem Solving2. The purpose of this paper is to report on the 2008 inaugural Equal Opportunities Conference held at the University of East Anglia, Norwich

3. Strategic Investment and Market Integration

4. PRIORITIES IN THE CHANGING WORLD OF AGRICULTURE

5. HEDONIC PRICES IN THE MALTING BARLEY MARKET

6. Wettbewerbs- und Industriepolitik - EU-Integration als Dritter Weg?

7. The Interest Rate-Exchange Rate Link in the Mexican Float

8. An institutional analysis of sasi laut in Maluku, Indonesia

9. The name is absent

10. The name is absent