I + B = Co + Ci / (1 + rt) — (1 + гь)В / (1 + rt)

(6)

where rb is the cost of borrowed capital and rt is the individual’s discount factor, which

takes into account the individual’s risk aversion or intertemporal impatience.

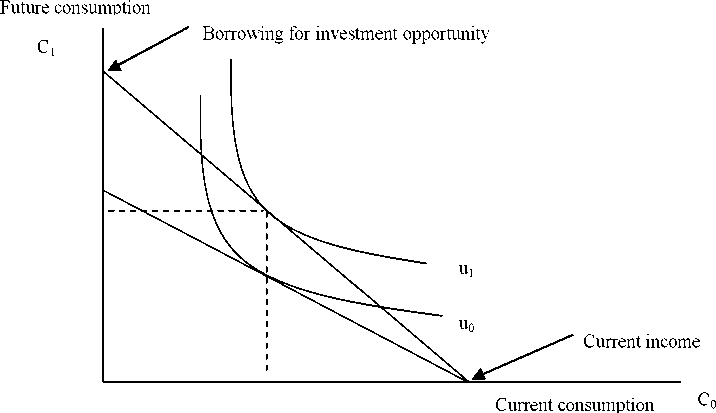

A common source of the demand for loanable funds is entrepreneurs wanting to

take advantage of business opportunities. Consider a situation in which investment

opportunities are too costly to be financed out of current income. That is, I - C0 for an

individual is small. The borrowed funds B are spent on a risky investment project which

yields returns at a rate r1. The utility maximizer can attain a higher indifference curve (u1)

when borrowing to invest in opportunities that allow higher future consumption. When

the investment outcome is successful, lenders receive the borrowed principal (B) plus

interest (at the prior agreed rate, rb). The investor has greater consumption possibilities in

the future, as seen by the outward shift of the vertical intercept in the budget line (figure

2).

Figure 2. Inter-temporal Utility Maximization with Borrowing

More intriguing information

1. The Context of Sense and Sensibility2. Rural-Urban Economic Disparities among China’s Elderly

3. The name is absent

4. Innovation Policy and the Economy, Volume 11

5. The name is absent

6. The name is absent

7. Mergers and the changing landscape of commercial banking (Part II)

8. Governance Control Mechanisms in Portuguese Agricultural Credit Cooperatives

9. The Employment Impact of Differences in Dmand and Production

10. The name is absent