4.2 - Model outcome and the role of regulation

As already said, we follow the Cox et al. (1979) model to investigate the impact of

different regulatory regimes onto NGN investment decisions. Its outcomes include

expected optimal investment timing and optimal investment policy (i.e. critical values)26.

Since the timing of the investment is of particular interest to policy makers and to national

sectors regulators, we will focus on the interval between when the investment opportunity

arises and when the investment is expected to be undertaken, named fugit. The central

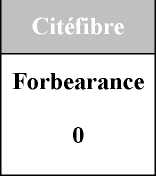

results of the simulations for the input data shown in Tables 1 and 2 are represented in

Figure 10.

Figure 10 - Number of years before the investment is undertaken

|

Established Operator | |

|

Forbearance |

Permanent regulation |

|

0 |

2.04 |

|

Sunset Clause |

Regulatory holiday |

|

1.95 |

0 |

For the sake of simplicity we divide the project lifespan into three phases. The first

phase includes the first six years of the project lifespan, which we define as the “volatile”

phase. The second phase (the “steady” phase) embraces years from the seven to the twelve,

while the third phase (the “terminal” one) includes the remaining years of the project

lifespan (from the thirteen to infinity). Differently from the steady and the terminal phases,

to refrain from the irreversible decision entails an insurance value in the volatile one.

26 Critical values can be used to determine the optimal subsidy i.e. the artificial increase of the NPV (either in

absolute term or expressed as a percentage) enabling a change of the today optimal policy outcome from

“delay the investment” to “invest now”.

29

More intriguing information

1. Tariff Escalation and Invasive Species Risk2. The name is absent

3. Publication of Foreign Exchange Statistics by the Central Bank of Chile

4. Strategic monetary policy in a monetary union with non-atomistic wage setters

5. Endogenous Determination of FDI Growth and Economic Growth:The OECD Case

6. Group cooperation, inclusion and disaffected pupils: some responses to informal learning in the music classroom

7. Biological Control of Giant Reed (Arundo donax): Economic Aspects

8. The name is absent

9. The name is absent

10. Moffett and rhetoric