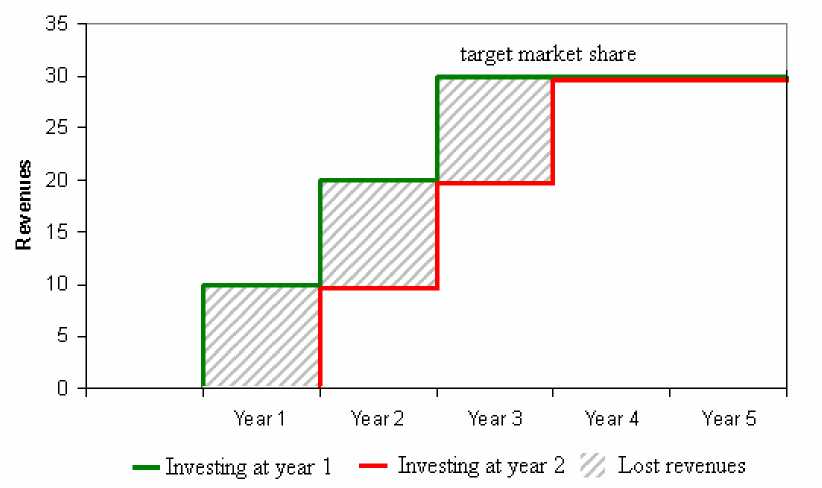

invested one year earlier (see Figure 9). Thus the value assigned to the payout variable in

the Citéfibre case is obtained by multiplying by three the foregone revenues suffered in the

period in which the decision to postpone was made.

Per unit up-front costs are estimated by resorting to a study of the investment costs of

NGN published the French telecommunications regulator Arcep (2006): the average cost

estimated by Arcep (€500) has been decreased to take into account that in Paris the roll-out

of the fibre is less expensive due to the possibility of exploiting the sewage system. A

sanity check of this value has been carried out by comparing with the value inferred

directly using Citéfibre available data. The up-front cost is therefore assumed to be equal to

€400.

Figure 9 - Revenues lost by investing one year later

The annualized volatility of the log return has been estimated using bi-weekly stock

returns. Since Citéfibre was floated on Euronext on the 2nd December 2005, the sample size

is slightly above 45 observations. A higher frequency would have increased the accuracy of

the estimate by increasing the number of observations; however this might have entailed an

24 Prior to December 2005 Citéfibre was not traded and thus this is the first market capitalisation availble.

26

More intriguing information

1. The name is absent2. Factores de alteração da composição da Despesa Pública: o caso norte-americano

3. Restricted Export Flexibility and Risk Management with Options and Futures

4. Optimal Rent Extraction in Pre-Industrial England and France – Default Risk and Monitoring Costs

5. The name is absent

6. The name is absent

7. The name is absent

8. The name is absent

9. Declining Discount Rates: Evidence from the UK

10. The name is absent