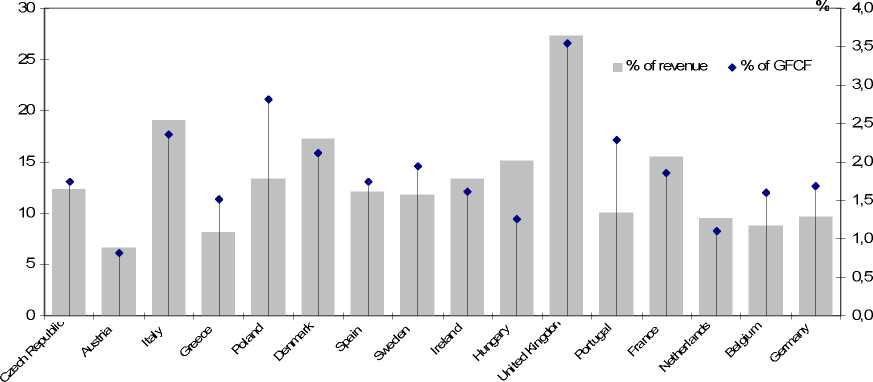

Figure 1 -Public telecommunication investment as a percentage of PTO revenue

and gross fixed capital formation (GFCF)

(2005)

Source: adapted from OECD (2007).

The slowdown in investment that dates back to the beginning of the decade is probably

coming to an end. On the one hand, the excess capacity that has characterised the decade as

a consequence of the massive build-up of transmission infrastructures from 1995 to 2000 is

finally being eroded by the dramatic increase in demand for broadband Internet4.

Broadband connections all over Europe have jumped from 52.6 million in 2005 to over 70

million in 2007 (European Commission, 2007a). On the other hand, the technological

paradigm is shifting. Differently from the leading ADSL technology, where traditional

analogue voice services and digital data transmission for Internet run over two different

platforms, in next generation networks voice (typically, voice over IP), music, videos and

all other sort of data are transported over the same integrated network.

4 According to standard definitions, broadband includes speeds over 125 megbits/secs, as compared to

traditional dial-up Internet which reaches 56 megs. In Europe (Eu 25) broadband connections are offered

mainly on copper twists through DSL technology. Other types of connections are modem cable (15%), optical

fiber (1%) and satellite (0,19%).

More intriguing information

1. Naïve Bayes vs. Decision Trees vs. Neural Networks in the Classification of Training Web Pages2. Female Empowerment: Impact of a Commitment Savings Product in the Philippines

3. Structural Breakpoints in Volatility in International Markets

4. The name is absent

5. El Mercosur y la integración económica global

6. Errors in recorded security prices and the turn-of-the year effect

7. Output Effects of Agri-environmental Programs of the EU

8. Consciousness, cognition, and the hierarchy of context: extending the global neuronal workspace model

9. Gender stereotyping and wage discrimination among Italian graduates

10. Secondary stress in Brazilian Portuguese: the interplay between production and perception studies