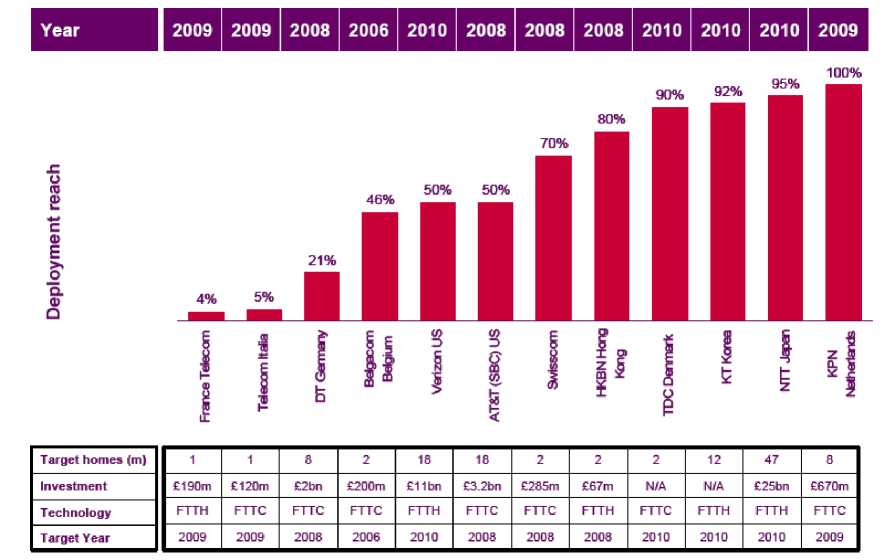

Figure 3 -Incumbent next generation access deployment plans by target date

Notes: in euro terms the amounts for each operator are: FT €273m, TI €172m, DT €2,8bn, Belgacom

€287, Verizon €16bn, AT&T €4,5bn, Swisscom €409m, HKBN €96m, NTT €36bn, KPN

€962m.

Source: adapted from Ofcom (2007).

The pace with which these potential benefits are realised will clearly depend on how

NGNs are regulated. The regulatory question for NGNs is quite well defined (its solution

less so, as we will see). Differently from the usual regulatory problem in

telecommunications - that is the opening up to competition of a legacy infrastructure, the

copper network, built during the monopoly years - the question here is how to define future

rules for networks which do not exist yet. The relevant trade off is between the incentive to

investment and the degree of competition in the future telecommunication market. On the

one hand, in fact, established operators, which will, inevitably, sustain most of the

investment in several countries, are waiting to see whether regulatory authorities decide to

5 See the European Commission recent Impact Assessment (European Commission, 2007b).

More intriguing information

1. Une nouvelle vision de l'économie (The knowledge society: a new approach of the economy)2. Dual Track Reforms: With and Without Losers

3. The Macroeconomic Determinants of Volatility in Precious Metals Markets

4. Trade Liberalization, Firm Performance and Labour Market Outcomes in the Developing World: What Can We Learn from Micro-LevelData?

5. An Incentive System for Salmonella Control in the Pork Supply Chain

6. Evaluating Consumer Usage of Nutritional Labeling: The Influence of Socio-Economic Characteristics

7. Determinants of Household Health Expenditure: Case of Urban Orissa

8. The name is absent

9. The Veblen-Gerschenkron Effect of FDI in Mezzogiorno and East Germany

10. THE INTERNATIONAL OUTLOOK FOR U.S. TOBACCO