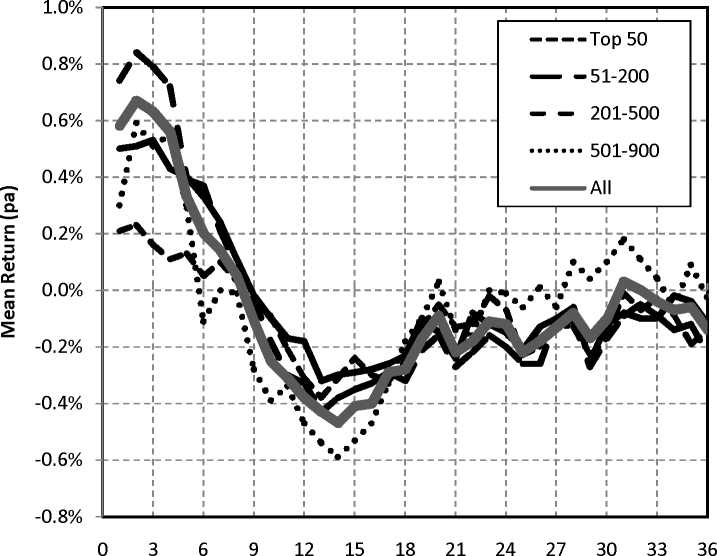

Holding Period (Months)

Figure 4 Mean monthly returns on a momentum portfolio formed by buying winners and

shorting the equally weighted portfolio of all stocks within the size cohort (1973-2004).

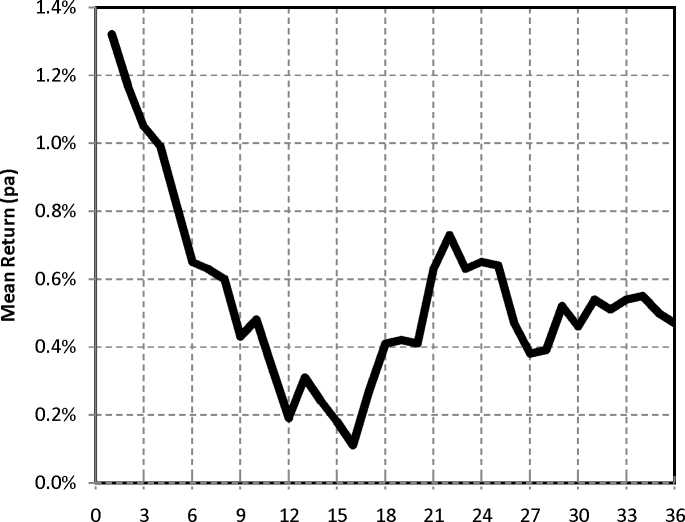

Holding Period (Months)

Figure 5 Mean monthly returns on a momentum portfolio formed from 9 size sorted portfolios

(1973-2004).

10

More intriguing information

1. Orientation discrimination in WS 22. The name is absent

3. Multifunctionality of Agriculture: An Inquiry Into the Complementarity Between Landscape Preservation and Food Security

4. Education Research Gender, Education and Development - A Partially Annotated and Selective Bibliography

5. IMPLICATIONS OF CHANGING AID PROGRAMS TO U.S. AGRICULTURE

6. STIMULATING COOPERATION AMONG FARMERS IN A POST-SOCIALIST ECONOMY: LESSONS FROM A PUBLIC-PRIVATE MARKETING PARTNERSHIP IN POLAND

7. Meat Slaughter and Processing Plants’ Traceability Levels Evidence From Iowa

8. The Role of Evidence in Establishing Trust in Repositories

9. Evaluation of the Development Potential of Russian Cities

10. Integrating the Structural Auction Approach and Traditional Measures of Market Power