|

Mnemonics |

Contents |

|

One Lag Unsaturated Model with No Simultaneous Dependence | |

|

012nl, |

Two Lag Unsaturated Model with No Simultaneous Dependence |

|

Cinu |

One Lag Saturated Model with No Simultaneous Dependence |

|

U1 |

One Lag Unsaturated Model |

|

U2 |

Two Lag Unsaturated Model |

|

S1 |

One Lag Saturated Model |

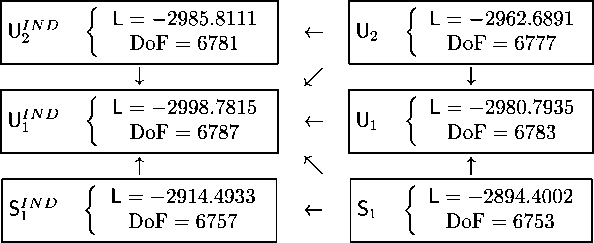

Table 1: Mnemonics for the estimated models

models, together with the degrees of freedom as reported in the following scheme:

The possible restrictions are indicated by an arrow connecting the two boxes:

in particular, if a box connects model Mt (U for unrestricted') to model Mh (R

for restricted), we say that model Mh is nested in model Mσ. Therefore, we

can test all the restrictions through a Likelihood Ratio test;15 in particular, if

we indicate by Ljy the log-likelihood of the unrestricted model and by the

log-likelihood of the model obtained after constraining some of the parameters,

the Likelihood Ratio test consists in calculating the statistic

2 ∙ (Lb - Lσ).

This statistic is asymptotically distributed as a where p is the number of pa-

rameters constrained in the restricted model. The results are reported in Table

3 and show that all the restrictions are refused at any conventional significance

level (90%, 95%, 99%). Clearly this procedure is not able to discriminate be-

tween two models that are not directly linked by a restriction, and therefore, we

cannot say whether U2 fits the data better than Si, since they are non-nested.

Therefore, in order to select a model, we calculate two widely used criteria for

the comparison of non-nested models: the AIC (Akaike Information Criterion)

and the BIC (Bayesian Information Criterion, due to Schwarz, 1978); in both

cases the model maximizing the criterion is selected. The formulas are the

—---------------

15See Gouriéroux, Monfort and Renault (1987) for a similar testing strategy.

19

More intriguing information

1. The name is absent2. Cyclical Changes in Short-Run Earnings Mobility in Canada, 1982-1996

3. Expectations, money, and the forecasting of inflation

4. The constitution and evolution of the stars

5. The name is absent

6. Constructing the Phylomemetic Tree Case of Study: Indonesian Tradition-Inspired Buildings

7. The name is absent

8. The name is absent

9. Foreign direct investment in the Indian telecommunications sector

10. AJAE Appendix: Willingness to Pay Versus Expected Consumption Value in Vickrey Auctions for New Experience Goods