Data for the three variables are the average value for the period 1985-1992. The analysis of

this period for the Spanish economy is specially relevant as it includes both an expansive

phase of the business cycle and a contractive one and also different monetary policy measures

(see annex 3). Averaging the data for explanatory variables is also appropriate, as we are

interested in analysing the average behaviour during the sample period. Averaging also

minimises the possibility that the results are affected by business-cycle dynamics (although

the average period is relatively short due to data availability). The data source for the relative

weights of manufacturing and building is Eurostat-Regio and data for the average firm size

come from DAISIE Annual industrial survey (New cronos). Both data are shown in annex 1.

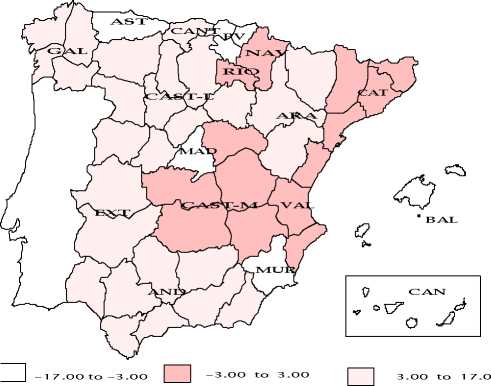

The obtained values of the indicator of the regional relative response to a common monetary

shock for the Spanish regions are also shown in annex 1 and are represented in figure 3. As it

can be seen regions with the highest response are the Mediterranean regions joint with

Castilla-La Mancha, Rioja and Navarra, while regions with the lowest response are Madrid,

Murcia and Cantabric regions. In general terms, the obtained classification is similar to the

one obtained by De Lucio and Izquierdo (1998). The proposed indicator has also been

calculated for different countries at a national level and the obtained results have been

compared with the ones by Carlino and DeFina (1998). As it can be seen in annex 2, both

results show that Ireland and Spain have greater responses to a common monetary shocks that

France, Italy and Netherlands.

Figure 3. Regional indicator of monetary policy relative responses

13

More intriguing information

1. Expectation Formation and Endogenous Fluctuations in Aggregate Demand2. The name is absent

3. The name is absent

4. Økonomisk teorihistorie - Overflødig information eller brugbar ballast?

5. Foreign Direct Investment and Unequal Regional Economic Growth in China

6. PER UNIT COSTS TO OWN AND OPERATE FARM MACHINERY

7. The name is absent

8. The Dictator and the Parties A Study on Policy Co-operation in Mineral Economies

9. The Institutional Determinants of Bilateral Trade Patterns

10. The name is absent