last point implies that the crash occurs independently of the true probability

of a drop next period, showing that the anticipation (together with the drop

of course) has driven the crash.

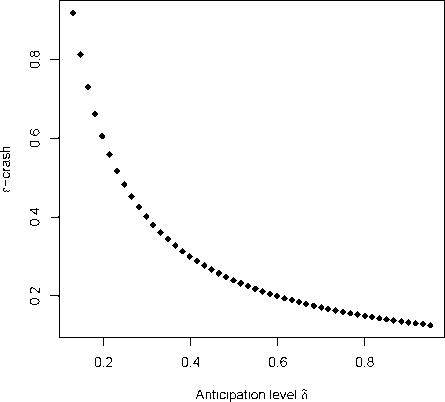

The next figure gives us a way to visualize the effect of drop anticipations

on the magnitude of a crash, given a particular drop of endowment next

period. We fix a 20% drop in the following simulation.

Figure 2: Crash magnitude as a function of the anticipation δ (α = 10)

Figure 2 provides the direct link between the magnitude of the crash and

the anticipation of the drop. Its main implication is that, for a fixed drop

of endowment, the higher the anticipation the higher the crash magnitude.

The intuition of this point is also given in the Introduction.

16

More intriguing information

1. Federal Tax-Transfer Policy and Intergovernmental Pre-Commitment2. PRIORITIES IN THE CHANGING WORLD OF AGRICULTURE

3. An Economic Analysis of Fresh Fruit and Vegetable Consumption: Implications for Overweight and Obesity among Higher- and Lower-Income Consumers

4. Party Groups and Policy Positions in the European Parliament

5. The name is absent

6. 03-01 "Read My Lips: More New Tax Cuts - The Distributional Impacts of Repealing Dividend Taxation"

7. Endogenous Heterogeneity in Strategic Models: Symmetry-breaking via Strategic Substitutes and Nonconcavities

8. ASSESSMENT OF MARKET RISK IN HOG PRODUCTION USING VALUE-AT-RISK AND EXTREME VALUE THEORY

9. Creating a 2000 IES-LFS Database in Stata

10. The name is absent