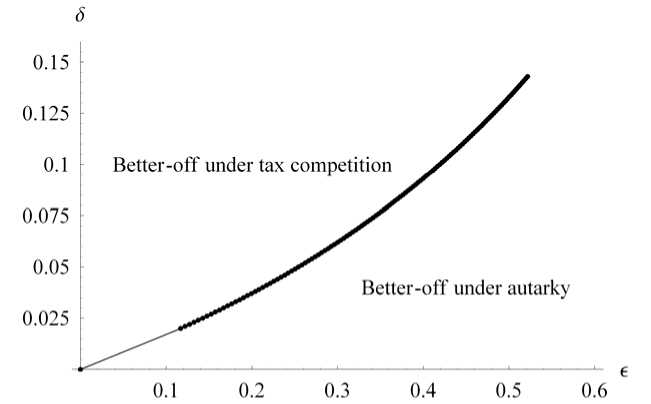

Figure 2: The borderline between welfare-increasing and welfare-reducing tax

competition (II)

the graphs in the two figures, tax competition is welfare-improving, whereas in

the area below the graphs it is welfare-reducing. As one would expect, the figures

illustrate that tax competition is more desirable the greater the political distortion

in favour of public sector voters.

The calibrated version of our model suggests that even a large political distor-

tion can only justify a moderate intensity of tax competition. For example, if the

public sector lobby is a trade union comprising 10 percent of the total work force

(αi = 0.1), the value of δ ≡ αi (pi - po) /po = 0.12 assumed in Table 1 would imply

pi /po = 2.2, that is, the political influence of a public sector insider would be more

than twice the influence of other voters, reflecting a very strong lobby. But even

in this case Table 1 indicates that the tax base elasticity will only have to exceed

0.3 before more intensive tax competition starts to reduce welfare, despite the

fact that further competition does not reduce public goods provision very much,

due to the low substitution elasticity 1∕σp = 1∕σg = 0.2 between private and

public goods. According to the present model tax competition thus seems a badly

targeted remedy against political distortions, compared to domestic institutional

reform such as restrictions on campaign contributions by lobby groups.

23

More intriguing information

1. Categorial Grammar and Discourse2. SOME ISSUES CONCERNING SPECIFICATION AND INTERPRETATION OF OUTDOOR RECREATION DEMAND MODELS

3. The name is absent

4. The name is absent

5. The Determinants of Individual Trade Policy Preferences: International Survey Evidence

6. Permanent and Transitory Policy Shocks in an Empirical Macro Model with Asymmetric Information

7. Food Prices and Overweight Patterns in Italy

8. Optimal Tax Policy when Firms are Internationally Mobile

9. The Variable-Rate Decision for Multiple Inputs with Multiple Management Zones

10. Corporate Taxation and Multinational Activity