ρ σ2 =0.00001

1 5 10 15 20 25 30 35 40

n=m

In----♦ Incentive Contract Market

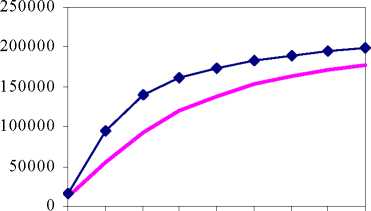

Figure 3. Comparing total certain equivalent with incentive contract and spot market

ρ σ2 =0.0001

1 5 10 15 20 25 30 35 40

n=m

Observing the figure 3 we see the processors may be either better off or worse off

using the incentive contract compared to the spot market depending on the

characteristics of the relationship involved. As agency theory predicts, an increase in the

magnitude of grower´s risk premium increases the appealing of the incentive contract

while decreasing the appealing of the spot market, considering the total certain

equivalent (see figure 3).

In the first best world with risk-neutral agents and/or absence of uncertainty

( ρσs2 =0), the incentive contract is rarely efficient, only when the number of operators is

reduced, nearly successive monopoly. However, in the second best world with risk-

averse growers, the spot market becomes less attractive due to the high risk premium

supported by the growers in this mechanism.

Then, as grower´s risk premium (i.e. risk aversion or output variance) increases,

relative preference for incentive contract is likely to increase over spot market. This

result is supported by other studies, for example Cheung (1969), Bardhan (1984) and

Parthasarthy and Prasad (1974).

Comparing the three figures, we can see cases in which the incentive contract

provides a smaller level of quality but a greater level of total certain equivalent than the

More intriguing information

1. The name is absent2. Computational Batik Motif Generation Innovation of Traditi onal Heritage by Fracta l Computation

3. Modelling Transport in an Interregional General Equilibrium Model with Externalities

4. The name is absent

5. Special and Differential Treatment in the WTO Agricultural Negotiations

6. Examining the Regional Aspect of Foreign Direct Investment to Developing Countries

7. The name is absent

8. DEVELOPING COLLABORATION IN RURAL POLICY: LESSONS FROM A STATE RURAL DEVELOPMENT COUNCIL

9. The effect of classroom diversity on tolerance and participation in England, Sweden and Germany

10. The name is absent