The Interest Rate-Exchange Rate Link in the Mexican Float

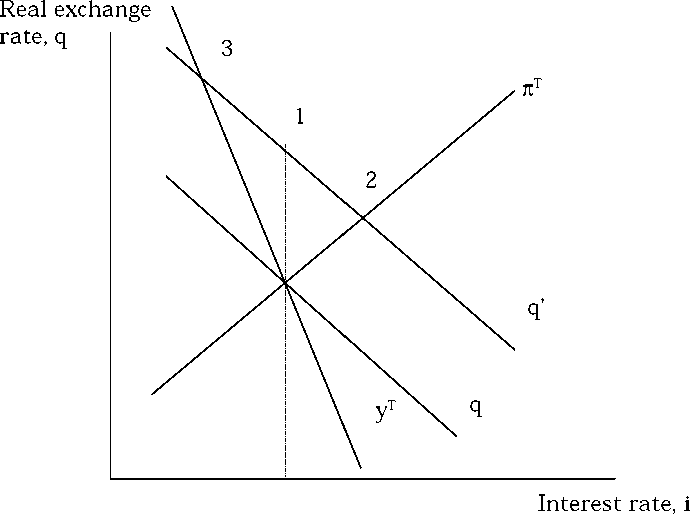

Figure 3. Output and inflation targets under contractionary

depreciation.

the rate of nominal currency depreciation (given that the inflation

rate will be increasing). But the higher depreciation rate will take

place in a context of falling interest rates. Both factors tend to depress

the return on peso investments, as shown by Equation (1). If private

agents are able to foresee this path, they will reduce their demand for

peso assets as they try to shift to dollar assets. This fall in the demand

for peso assets will make it difficult to follow an anti-cyclical policy. In

contrast, choosing a tighter policy stance after the capital account shock

will yield a declining rate of currency depreciation together with higher

interest rates. This combination will tend to stabilize the demand for

peso assets, which may be particularly important in the aftermath of

the shock (a point stressed by Carstens and Werner 1999, pp. 44, 47).

Perhaps it is important to clarify that this result does not depend

on the assumption that a currency depreciation has a negative output

effect, but only that output falls after a negative capital account shock

(for instance, because of the effect on financial aggregates following a

23

More intriguing information

1. The Effects of Attendance on Academic Performance: Panel Data Evidence for Introductory Microeconomics2. The Structure Performance Hypothesis and The Efficient Structure Performance Hypothesis-Revisited: The Case of Agribusiness Commodity and Food Products Truck Carriers in the South

3. Estimating the Impact of Medication on Diabetics' Diet and Lifestyle Choices

4. Examining the Regional Aspect of Foreign Direct Investment to Developing Countries

5. The name is absent

6. Climate change, mitigation and adaptation: the case of the Murray–Darling Basin in Australia

7. Innovation Policy and the Economy, Volume 11

8. How Offshoring Can Affect the Industries’ Skill Composition

9. Business Cycle Dynamics of a New Keynesian Overlapping Generations Model with Progressive Income Taxation

10. Survey of Literature on Covered and Uncovered Interest Parities