William Davidson Institute Working Paper 487

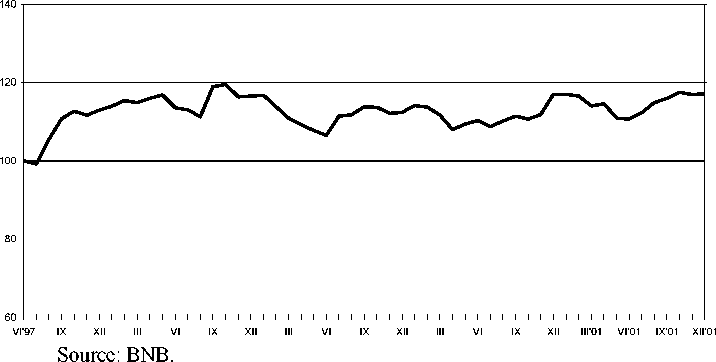

the Bulgarian lev is experiencing some moderate real appreciation28, which seems to be

somehow kept in limits (see Figure 11).

Figure. 11. Real effective exchange rate appreciation index

In fact Bulgarian monetary authorities do not have much room for maneuver in

order to alleviate the effect of the real exchange rate appreciation. Taking into

consideration the possible unfavorable consequences to expectations and economic

behavior of an eventual exchange rate regime shift, the potential for exchange rate

overshooting and the existence of price and wage rigidity, Bulgaria has no choice of

strategies but keeping stable nominal exchange rate with somewhat higher inflation29.

On the side of the real economy, new efforts should be put in completing

privatization and price liberalization. Further steps, typical for the catching-up process

should be taken in respect to wage setting and making the labor market more flexible,

establishing productivity-enhancing domestic and foreign investment, and efficient credit

28 The Real Effective Exchange Rate Index is calculated as a basket of the three currencies with the

largest share in the trade turnover: USD - 57.24%, DEM - 41.98%, CHF - 0.71%. Consumer prices

are used as a measure to deflate the nominal exchange rates.

29 For the range of issues under discussion before the monetary authorities of the accession countries

undertake some strategy to cope with real appreciation see Backe and al., 2002.

26

More intriguing information

1. NATIONAL PERSPECTIVE2. EU enlargement and environmental policy

3. Skills, Partnerships and Tenancy in Sri Lankan Rice Farms

4. Income Taxation when Markets are Incomplete

5. On Dictatorship, Economic Development and Stability

6. The name is absent

7. Integration, Regional Specialization and Growth Differentials in EU Acceding Countries: Evidence from Hungary

8. The name is absent

9. DEMAND FOR MEAT AND FISH PRODUCTS IN KOREA

10. Wounds and reinscriptions: schools, sexualities and performative subjects