As a benchmark case, consider first the optimal tax policy with respect to the

tax rate and the tax base when firms are immobile.

3.4 Optimal tax policy with immobile firms

With Ah > A+, the welfare function becomes

W = U ^j У [F (1 - u) - (1 - au) K] dAdB^ +H ^j ʃ и (F

- aK) dAdB

(18)

with F = F (K, A, B) for simplicity, subject to

F(K,Al) (1 - и) - (1 - au) K = 0 (19)

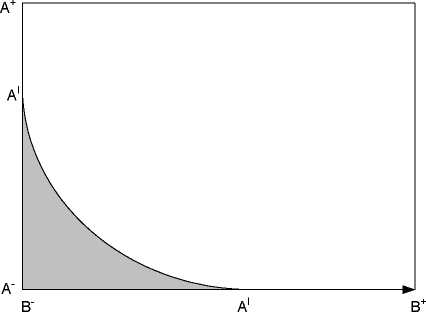

for every given level of B. Figure 1 shows the two-dimensional profitability

space of the firms in the economy:

Figure 1: Immobile firms.

The firms in the shaded left bottom corner are not profitable enough and do not

produce. Firms in the white area do produce and can be taxed. Firms along the Al

frontier are indifferent between producing and leaving the market. By increasing

(lowering) the effective tax burden, the government shifts the Al frontier to the

lower left (upper right).

The optimality conditions with respect to u and a are:

10

More intriguing information

1. SAEA EDITOR'S REPORT, FEBRUARY 19882. The name is absent

3. New Evidence on the Puzzles. Results from Agnostic Identification on Monetary Policy and Exchange Rates.

4. Testing Hypotheses in an I(2) Model with Applications to the Persistent Long Swings in the Dmk/$ Rate

5. Consumption Behaviour in Zambia: The Link to Poverty Alleviation?

6. AN EXPLORATION OF THE NEED FOR AND COST OF SELECTED TRADE FACILITATION MEASURES IN ASIA AND THE PACIFIC IN THE CONTEXT OF THE WTO NEGOTIATIONS

7. Errors in recorded security prices and the turn-of-the year effect

8. The name is absent

9. Convergence in TFP among Italian Regions - Panel Unit Roots with Heterogeneity and Cross Sectional Dependence

10. Needing to be ‘in the know’: strategies of subordination used by 10-11 year old school boys