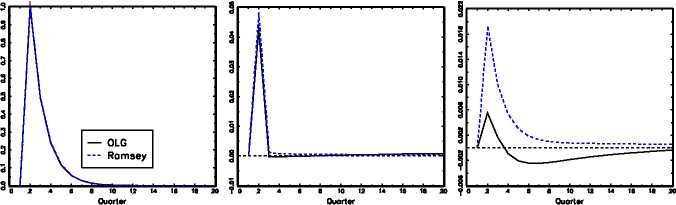

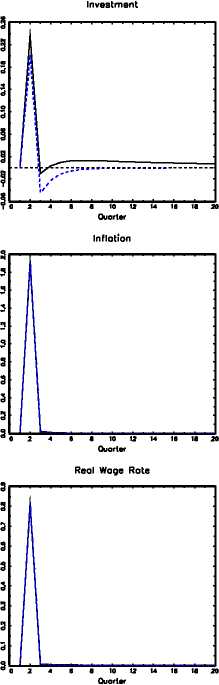

Figure 7

Monetary Shock in the Representative Agent Economy

Thetahut

Output

Consumption

Real Interest Rate

O 2 Л в β 10 U U le 18 20

Ouorlar

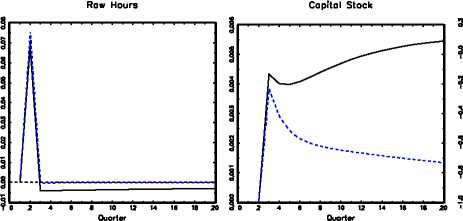

stock remains above its non-stochastic level for many quarters.

We conclude this section by a comparison of the time series properties of the OLG and

the Ramsey model. For this purpose we compute 100 simulations of 150 periods length

each17 and filter each simulated time series using the HP-filter with weight 1,600. The

time series moments reported in Table 2 are averages over the 100 simulations. The

technology shock and the growth shock are generated by the processes (14) and (18),

respectively. We use the same sequence of shocks for the OLG and the Ramsey model.

The first column in Table 2 presents the aggregate variable. In the second and fifth

column, the standard deviation of the respective variables are displayed. Columns 3 and

6 display the correlation with output, while columns 4 and 7 present the autocorrelation

of the variables in the two models, respectively.

17See, e.g., Cooley and Hansen (1995), p. 189.

23

More intriguing information

1. What Lessons for Economic Development Can We Draw from the Champagne Fairs?2. Self-Help Groups and Income Generation in the Informal Settlements of Nairobi

3. Apprenticeships in the UK: from the industrial-relation via market-led and social inclusion models

4. Learning-by-Exporting? Firm-Level Evidence for UK Manufacturing and Services Sectors

5. Delayed Manifestation of T ransurethral Syndrome as a Complication of T ransurethral Prostatic Resection

6. The name is absent

7. Visual Artists Between Cultural Demand and Economic Subsistence. Empirical Findings From Berlin.

8. The name is absent

9. ADJUSTMENT TO GLOBALISATION: A STUDY OF THE FOOTWEAR INDUSTRY IN EUROPE

10. The name is absent