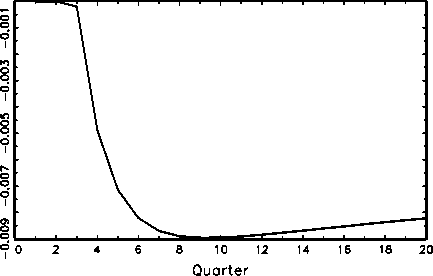

Gini wealth

Figure 6

Monetary shock in the OLG model and distribution

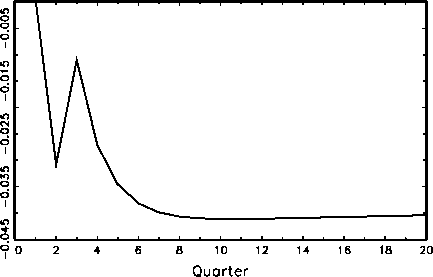

Gini capital Gini money

Gini market∕disposable income

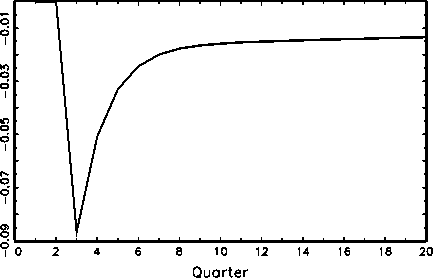

of capital services. Again, the transfer and tax system more than compensates these

effects. Since the real value of pensions sharply declines in first period of the shock

transfers sore by more than 30 percent. In the next four periods transfers are still well

above 1 percent as compared to their non-stochastic long run level. The additional wage

and capital income of the richer agents is taxed at a higher rate. As a consequence of

both effects the distribution of disposable income becomes more equal.

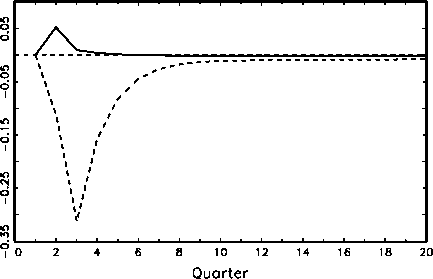

The impulse response functions of the aggregate variables in the Ramsey model with

Calvo price staggering are graphed in Figure 7 (the dotted lines). Again the ordering

of the variables is identical to the one in Figure 5. Notice that the qualitative behavior

of the variables in response to a monetary expansion is the same in the two economies

for all variables with a minor exception. In the OLG model, there is a little more

consumption smoothing than in the representative-agent economy so that the capital

22

More intriguing information

1. The name is absent2. Eigentumsrechtliche Dezentralisierung und institutioneller Wettbewerb

3. Individual tradable permit market and traffic congestion: An experimental study

4. Monetary Discretion, Pricing Complementarity and Dynamic Multiple Equilibria

5. The name is absent

6. A Theoretical Growth Model for Ireland

7. The Prohibition of the Proposed Springer-ProSiebenSat.1-Merger: How much Economics in German Merger Control?

8. Institutions, Social Norms, and Bargaining Power: An Analysis of Individual Leisure Time in Couple Households

9. Cancer-related electronic support groups as navigation-aids: Overcoming geographic barriers

10. The name is absent