19

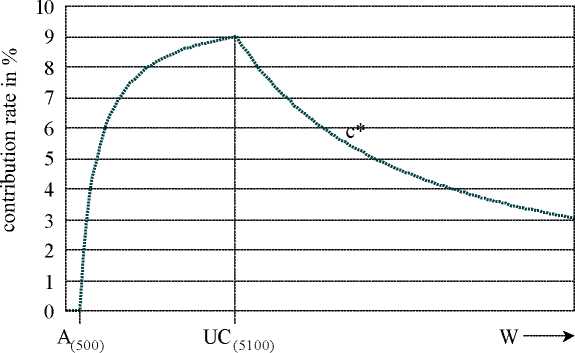

Overview 5: Effective contribution rate in case of an allowance

A = allowance (500)

UC = upper ceiling (5100)

c = contributi on rate (10 %)

W = (individua l) gross earnings

= effective (individua l) contributi on rate

_ c (W - A )

= W

for W ≤ UC

Disentangling employee’s and employer’s contributions - which would result from the above

mentioned two strategies (different contribution rates or allowances) - could stimulate (at

least in Germany) a more fundamental discussion about the assessment base for employer’s

contributions. This was discussed in Germany (as well as in some other European countries

like Austria and Belgium) in the past. It was proposed not to base employer’s contributions on

earnings only but on (gross or net) value added of the firm. Because of the different ratios of

labour costs to value added in different branches of the economy contribution payments

based only on earnings are burdening in particular labour-intensive production.15 Such a value

added levy of employers, however, would in fact be a tax that cannot be allocated to the

individual employee as in case of earnings-related employer’s contributions which are part of

15 For a detailed analysis see Schmahl et al. (1984) and Schmahl (1992).

More intriguing information

1. Foreword: Special Issue on Invasive Species2. Antidote Stocking at Hospitals in North Palestine

3. Prevalence of exclusive breastfeeding and its determinants in first 6 months of life: A prospective study

4. How Low Business Tax Rates Attract Multinational Headquarters: Municipality-Level Evidence from Germany

5. Pass-through of external shocks along the pricing chain: A panel estimation approach for the euro area

6. American trade policy towards Sub Saharan Africa –- a meta analysis of AGOA

7. The name is absent

8. The name is absent

9. The name is absent

10. The name is absent