s12

pp and

1975 1980 1985 1990 1995 2000

2-Pdf

their heterogeneous exchange rate forecasts are assumed to follow random walks with

drift. With this assumption, revisions of market participants’ forecasting strategies

lead to temporally unstable drift terms in the processes driving the endogenous vari-

ables of the model. FGJ show that these broken-trends processes can be approximated

as I(2).

6 Specification of deterministic terms in the empir-

ical model

A proper specification of deterministic terms in the I(2) model is mandatory for the

model to yield statistically good estimates. From (8) we know that linear trends in the

data can originate from several sources: (l) E(∆x^t) = 0 implying that some of the

variables have exhibited significant linear growth over the sample period, (2) E(β'xt) =

p0t = 0 implying that some of the cointegration relations are trend-stationary, (3) from

initial conditions. Even though one would expect a linear trend to be present in

nominal prices (reflecting the fact that average inflation rates have been nonzero in

most economies) it is less obvious that one should expect a linear trend in relative

prices and nominal exchange rates. Since deterministic trends in p1,t and p2,t are likely

to cancel in p1jt— p2,t, one should generally expect the deterministic components to be

different in a model for p1,t, p2,t, and s12,t as compared to a model for ppt = p1,t — p2,t

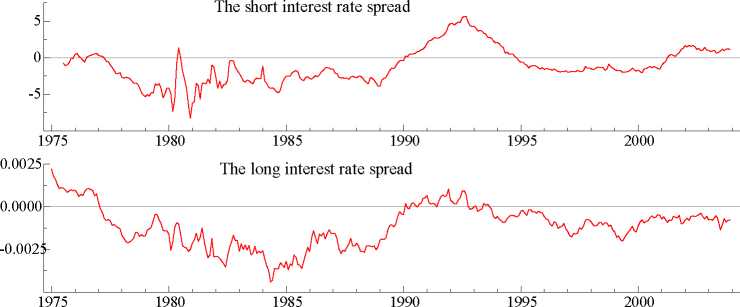

and s12,t. The graph in Figure l shows a downward sloping trend in relative prices

12

More intriguing information

1. SME'S SUPPORT AND REGIONAL POLICY IN EU - THE NORTE-LITORAL PORTUGUESE EXPERIENCE2. The name is absent

3. FASTER TRAINING IN NONLINEAR ICA USING MISEP

4. The name is absent

5. Hemmnisse für die Vernetzungen von Wissenschaft und Wirtschaft abbauen

6. The name is absent

7. Nurses' retention and hospital characteristics in New South Wales, CHERE Discussion Paper No 52

8. Short Term Memory May Be the Depletion of the Readily Releasable Pool of Presynaptic Neurotransmitter Vesicles

9. The name is absent

10. Tobacco and Alcohol: Complements or Substitutes? - A Statistical Guinea Pig Approach