0.61

The Evolution of Output when

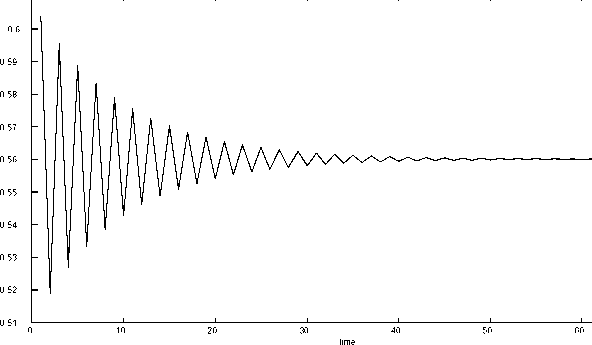

ψ <1.

Figure 3: The Evolution of Output when ψ < 1.

variables. The situation is different when condition (34) is violated. This case

is dealt with next.

Case 2 Assume that the parameters of the model satisfy the following inequality

ψ > 1, (35)

i.e., assume that whenever agents choose to form expectations in an adaptive

manner the level of capital stock, and hence the marginal propensity to save,

follow an explosive path.4

Condition (35) implies that at any time the economy can be in either of two

regimes. For q'f sufficiently close to one it follows a process that converges to an

equilibrium, i.e., the economy could be in a convergence regime. On the other

hand for q2 sufficiently close to zero the economy follows a process that does not

converge to an equilibrium, i.e., the economy is in a divergence regime. Figure

(4) illustrates sample dynamics in the two regimes.

In general, the economy could be in either of the two regimes depending

on the precise value of q2. Recall that q2 does not constitute a parameter of

the economy, but it depends on actions taken by economic agents and is itself

determined as an equilibrium outcome. In particular, if economic agents choose

q2 to be large enough then the economy will follow a convergent path, on the

other hand, if they choose q2 to be small then the economy will proceed on a

divergent path.

4Assumption of case 2 can be derived rather than imposed in a model in which optimization

costs accrue in the form of forgone profits rather than in the form of utility costs.

20

More intriguing information

1. Female Empowerment: Impact of a Commitment Savings Product in the Philippines2. AN EMPIRICAL INVESTIGATION OF THE PRODUCTION EFFECTS OF ADOPTING GM SEED TECHNOLOGY: THE CASE OF FARMERS IN ARGENTINA

3. Eigentumsrechtliche Dezentralisierung und institutioneller Wettbewerb

4. Elicited bid functions in (a)symmetric first-price auctions

5. Towards Learning Affective Body Gesture

6. The name is absent

7. The name is absent

8. The name is absent

9. On s-additive robust representation of convex risk measures for unbounded financial positions in the presence of uncertainty about the market model

10. Imputing Dairy Producers' Quota Discount Rate Using the Individual Export Milk Program in Quebec