1.5 Estimation of parameters

11

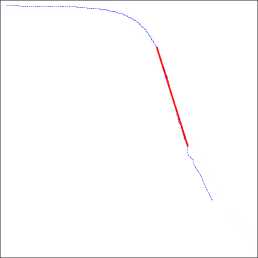

Sample of size N=10^4

-4 -2 0 2 4

log(x)

Figure 1.4: A double logarithmic plot of the right tail of an empirical symmetric

1.9-stable distribution function for a sample of size N = 104 (left

panel) and N = 106 (right panel). Thick red lines represent the

linear regression fit. The tail index estimate (<^ = 3.7320) obtained

for the smaller sample is close to the initial power-law like decay of

the larger sample (<^ = 3.7881). The far tail estimate α = 1.9309 is

close to the true value of α.

θ STFstab04.xpl

i.e. the negative tail) observations, after a crossover from a temporary power-

like decay (which surprisingly indicates α ≈ 3.7). Moreover, the obtained

estimates still have a slight positive bias, which suggests that perhaps even

larger samples than 106 observations should be used. In Figure 1.4 we used

only the upper 0.15% of the records to estimate the true tail exponent. In

general, the choice of the observations used in the regression is subjective and

can yield large estimation errors, a fact which is often neglected in the literature.

A well known method for estimating the tail index that does not assume a

parametric form for the entire distribution function, but focuses only on the

tail behavior was proposed by Hill (1975). The Hill estimator is used to estimate

the tail index α, when the upper (or lower) tail of the distribution is of the

form: 1 - F (x) = Cx-α, see Figure 1.5. Like the log-log regression method, the

Hill estimator tends to overestimate the tail exponent of the stable distribution

More intriguing information

1. The name is absent2. Spatial agglomeration and business groups: new evidence from Italian industrial districts

3. The name is absent

4. The name is absent

5. Design and investigation of scalable multicast recursive protocols for wired and wireless ad hoc networks

6. Epistemology and conceptual resources for the development of learning technologies

7. EU Preferential Partners in Search of New Policy Strategies for Agriculture: The Case of Citrus Sector in Trinidad and Tobago

8. Geography, Health, and Demo-Economic Development

9. The name is absent

10. Government spending composition, technical change and wage inequality