and that VT1,3(x,y) = (2.27; 4.84; 6.86) and VT3,2(x,y) = (2.46; 4.58; 6.92) are not LD-comparable,

although labor and capital tax schedules are separately comparable by ψ(x) and ψ(y), and

also using the Lorenz Domination criterium. Although income distribution of this example is

not dense, we obtain exactly what Jakobbson (1976) predicts (see Calonge and Tejada, 2009,

for a further argument on how density of can affect Jakobsson results).

In conclusion, if Condition 1 does not hold, dual tax cuts T1,3 and T3,2 cannot be compared,

neither by ψ(x+y) nor ψ (x,y) nor using the Lorenz Domination criterium on the total post-

tax income distribution, as it is the case when such condition does hold. Therefore, Condition

1 is necessary. Similar examples show that Condition 2 also necessary.

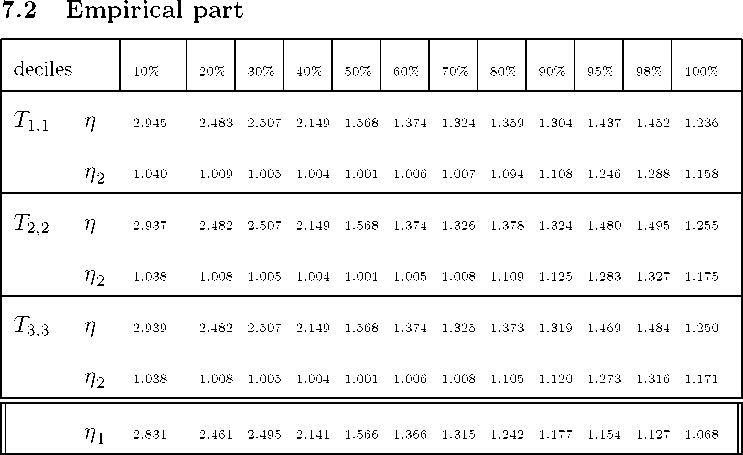

Table A.3. Losers and gainers analysis: elasticities.

References

[1] Arcarons, J., Calonge, S. (2004). ”Modelo de Microsimulacion SIMESP v4.0 (O® B-

3916-08”. e-publica.

35

More intriguing information

1. Innovation and business performance - a provisional multi-regional analysis2. Behavior-Based Early Language Development on a Humanoid Robot

3. Wettbewerbs- und Industriepolitik - EU-Integration als Dritter Weg?

4. On the origin of the cumulative semantic inhibition effect

5. The name is absent

6. Estimating the Technology of Cognitive and Noncognitive Skill Formation

7. ANTI-COMPETITIVE FINANCIAL CONTRACTING: THE DESIGN OF FINANCIAL CLAIMS.

8. Sectoral specialisation in the EU a macroeconomic perspective

9. Reconsidering the value of pupil attitudes to studying post-16: a caution for Paul Croll

10. The name is absent