provided by Research Papers in Economics

ESSAYS ON ISSUES

THE FEDERAL RESERVE BANK

FEBRUARY 2000

OF CHICAGO

NUMBER 150

Chicago Fed Letter

Mergers and the changing

landscape of commercial

banking (Part II)

In a recent Chicago Fed Letter, I exam-

ined the motivations for, and the con-

sequences of, the tremendous wave of

U.S. bank mergers during the 1980s

and 1990s.1 In that document I reached

three main conclusions. First, I argued

there is little evidence of any systemat-

ic reduction in competition in retail

banking or small business financing

markets as a result of the bank merger

wave. Although the largest commercial

banks have a much more prominent

national position today than 20 years

ago, these banks’ shares of local banking

markets have not increased materially.

Second, I suggested that the current

bank merger wave is showing signs of

maturing. A number of commercial

banks have achieved nationwide or

near-nationwide geographic coverage,

and as additional banks attain this

geographic scope the demand for

large market extension mergers will

naturally diminish. Furthermore, the

rapid development of the Internet

and e-commerce may allow banks to

replace, or at least complement, their

merger-based growth strategies with

internal growth via electronic distribu-

tion of financial services. Since Part I

was written, the Financial Institutions

Modernization Act (FIMA) of 1999

abolished the historical separation

of commercial banking, investment

banking, and insurance underwriting.

This long-awaited development will

likely dampen the bank merger wave

further, as acquisitive banks shift their

focus—and their scarce acquisition

capital—away from purchasing other

banks and toward purchasing insurance

companies and securities firms.

Third, I indicated that from our van-

tage point at the end of the 1990s,

it may be too early to evaluate the

eventual competitive implications of

the bank merger wave. If fully success-

ful, the electronic delivery of retail

and wholesale banking services may

make the notion of “local” banking

markets obsolete. To the degree that

this happens—and to the degree

that large banks can limit the entry

and/or the mobility of small banks in

electronic markets—the increasing

national market shares of large com-

mercial banks may have more serious

competitive implications than is gen-

erally thought.

In this Fed Letter, I discuss the prospects

for small commercial banks in a post-

merger-wave banking industry in which

electronic delivery of financial services

becomes commonplace. In such a

world, should we expect “branchless”

delivery of financial services to be

dominated by a few large banks, or

will the advent of electronic banking

markets provide important strategic

opportunities for small banks? I pro-

pose a simple conceptual framework

for thinking about this question, a

framework that considers the strate-

gic advantages and disadvantages of

increased bank size.

Local versus national

banking markets

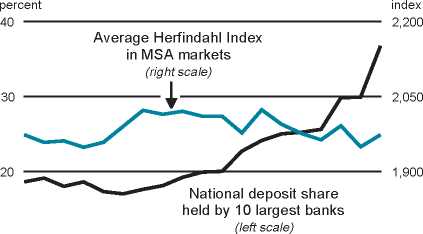

Between 1980 and 1998

the share of domestic de-

posits held by the nation’s

ten largest commercial

banks nearly doubled.

Large banks achieved

this growth primarily by

making market extension

mergers, which change

the ownership of the

acquired bank without

affecting the structure

of local banking markets.

As seen in figure 1 (which

is reprinted here from

Part I of this Fed Letter),

the national market

shares of large banks increased mark-

edly during the bank merger wave but

the concentration of local banking

markets remained stable. Hence, by

traditional measures of market struc-

ture, 20 years of bank mergers had lit-

tle adverse impact on competitive

conditions in U.S. commercial bank-

ing markets.

But these structural changes occurred

during the traditional “brick and mor-

tar” banking paradigm, in which most

retail banking and small business

banking services were provided by lo-

cal banks in local markets. Today, a

growing number of household and

business customers access account in-

formation, transfer funds, pay bills,

make trades, and apply for loans elec-

tronically, without ever setting foot in

a branch office. The banking industry

may be in the midst of a paradigm shift,

in which electronic delivery channels

and automated lending technology will

increasingly allow out-of-market banks

to compete for retail and small busi-

ness customers without establishing a

physical presence in the local market.

No one knows for sure how electronic

delivery channels will ultimately alter

the banking landscape, but some

1. National and local market structure

10...................1,750

1980 ’82 ’84 ’86 ’88 ’90 ’92 ’94 ’96 ’98

Note: HHI = sum of squared market shares of all banks in market.

Source: Board of Governors of the Federal Reserve System.