Journal of Applied Economic Sciences

VolumeI_Issue1 (1)_2006

Economic environment

Founding of decisions

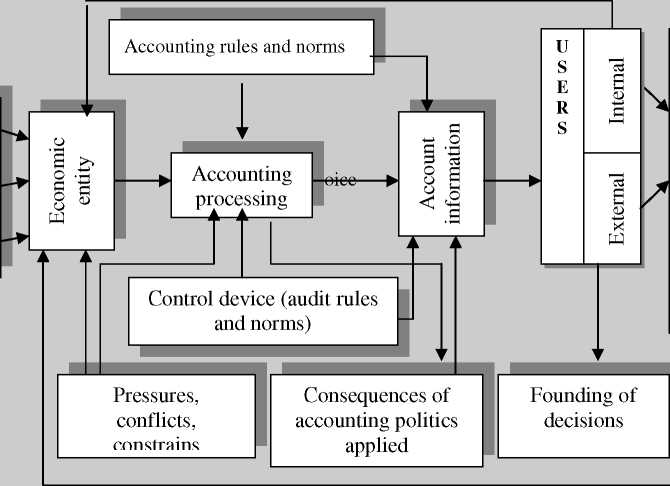

Figure 3. Accounting as social intermediation instrument

Along its evolution the accounting had to find solutions and to adapt to the economic reality,

fact which leaded to the use of some notions and accounting terms, and also to the occurrence and

appliance of some rules and conventions in order to obtain the information. So, the accounting has

became today a complex technique of registration and reflection of economic-financial reality, an

informational system adjusted to the users needs, an administration and communication instrument

which provides the company integration and dialogue with its external environment.3

Accounting has as scope to measure and transpose in a proper language one entity activities, but

this process is directly affected by its specific rules and norms, which are, in their turn, the results of

elements (factors) like culture, economic development, history, institutions capable to establish these

types of rules etc. The company relationships with the environment where they perform their activity

generate the need of relevant and objective information, of which satisfaction needs an adequate offer.

The production of account information is provided by the specialists practitioners in the area, a

process performed organized, inside the accounting informational system of economic entities. This

type of information must have to satisfy certain needs, so to have utility for all the ones making up the

category of users of accounting products, a fact for which their submission must be built in a dynamic

and rational process, result of the negotiations and compromises between the company and the

external factors. Beside, the market of account information represents the way to confront and regulate

the offer and the request in this area. In this context the offer denotes the total information obtained

inside the accounting system, and also the forms and methods to distribute them, while, on the other

side of the barricade, the request is being represented by the users’ informational needs of this type of

products, and also by the pressure they lay over the generating system.

As we previously noted, the informational offer is the assembly of information available for

different groups of users, to this component of the communication process and capitalization of the

products of accounting system being attached the concept of producer (tenderer) of account

information. The inclusion area for this type of offer is relatively ample, the financial communication

to different users being performed on different ways. Even if the methods to communicate the

3 Minu, M., (2002), Accounting as power instrument, Economic Publishing House, Bucharest, pp. 145.

17

More intriguing information

1. The demand for urban transport: An application of discrete choice model for Cadiz2. The name is absent

3. The name is absent

4. Fiscal Reform and Monetary Union in West Africa

5. The name is absent

6. The Advantage of Cooperatives under Asymmetric Cost Information

7. Neighborhood Effects, Public Housing and Unemployment in France

8. The duration of fixed exchange rate regimes

9. Keynesian Dynamics and the Wage-Price Spiral:Estimating a Baseline Disequilibrium Approach

10. The name is absent