because the information necessary is already reflected in the current account. This is based on

Campbell and Shiller’s (1987) work on savings and income.

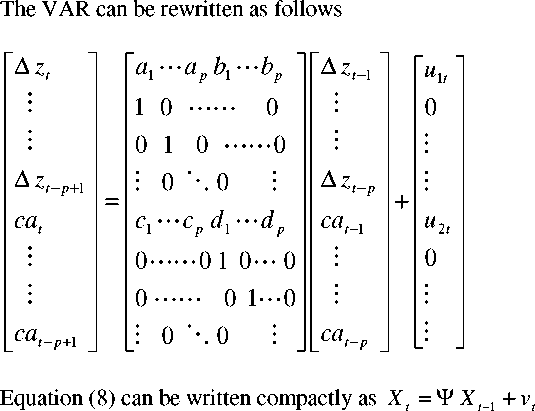

We estimate unrestricted bivariate vector auto regression (VAR) of changes in national cash

flow and the actual consumption smoothing current account given by the following

δ Zt

cat

a ( L ) b ( L ) Jδ Zt-1

c ( L ) d ( L ) ɪ cat-1

(7)

where ∆zt =∆( qt - it - gt ) is the change in national cash flow, cat is the actual consumption

smoothing current account which equals yt - it - gt - θct (analogous to equation (5) of the

optimal current account), a (L), b (L), c (L) and d (L) are polynomials in the lag operator of order p,

and u 11 and u21 are errors with a conditional mean of zero.

(8)

|

■ |

■a 1 1 |

0 |

ap b1 ...... |

. bP ~ |

■ u 1, 1 | |||

|

M |

0 |

1 |

0 L |

L0 |

M | |||

|

b V where X, = t |

cazt-p+ |

, ψ= |

≡ c1 |

0 |

O 0 c d 1 |

M Ld Lp |

and vt = |

M u 21 |

|

: |

0∙ |

... |

l0 1 |

0L 0 |

0 | |||

|

: |

0 |

.. |

. L 0 |

1L 0 |

m | |||

|

_ cat - p+1 _ |

_m |

0 |

O 0 |

M _ |

Lm J |

More intriguing information

1. Ahorro y crecimiento: alguna evidencia para la economía argentina, 1970-20042. Business Cycle Dynamics of a New Keynesian Overlapping Generations Model with Progressive Income Taxation

3. Volunteering and the Strategic Value of Ignorance

4. WP 48 - Population ageing in the Netherlands: Demographic and financial arguments for a balanced approach

5. The name is absent

6. The name is absent

7. MANAGEMENT PRACTICES ON VIRGINIA DAIRY FARMS

8. Evidence of coevolution in multi-objective evolutionary algorithms

9. A Bayesian approach to analyze regional elasticities

10. Effects of red light and loud noise on the rate at which monkeys sample the sensory environment