Risk

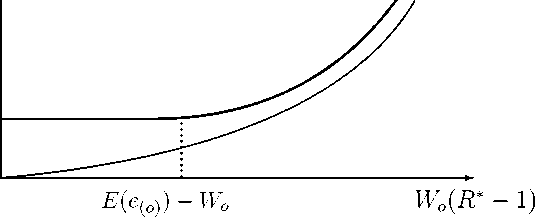

Fig.l The risk-value efficient frontier depicts the minimal portfolio risk as a func-

tion of the required expected portfolio return R*. The thin curve represents

the frontier for an endogenous benchmark, the thick curve for an exogenous

benchmark.

3.2 Risk-Value Models With an Exogenous Benchmark

Now consider risk functions with an exogenous benchmark e; e ≥0. Then in

the first order condition (8) for a risk-value efficient portfolio the second term

disappears since portfolio choice has no effect on the benchmark. Hence the

first order condition reads:

-f (⅛) = ηπ, + A; Vε.

(l2)

Again, A > 0 so that η < 0 follows.

Taking expectations yields

-E [f (e)] = η + A (l3)

so that subtraction of (l2) from (l3) leads to

-E[f (e)] + f (eε) = ηθε; V ε. (l4)

l5

More intriguing information

1. The Value of Cultural Heritage Sites in Armenia: Evidence From a Travel Cost Method Study2. CROSS-COMMODITY PERSPECTIVE ON CONTRACTING: EVIDENCE FROM MISSISSIPPI

3. What Lessons for Economic Development Can We Draw from the Champagne Fairs?

4. A COMPARATIVE STUDY OF ALTERNATIVE ECONOMETRIC PACKAGES: AN APPLICATION TO ITALIAN DEPOSIT INTEREST RATES

5. A Rational Analysis of Alternating Search and Reflection Strategies in Problem Solving

6. The name is absent

7. The name is absent

8. ISO 9000 -- A MARKETING TOOL FOR U.S. AGRIBUSINESS

9. ‘Goodwill is not enough’

10. PRIORITIES IN THE CHANGING WORLD OF AGRICULTURE