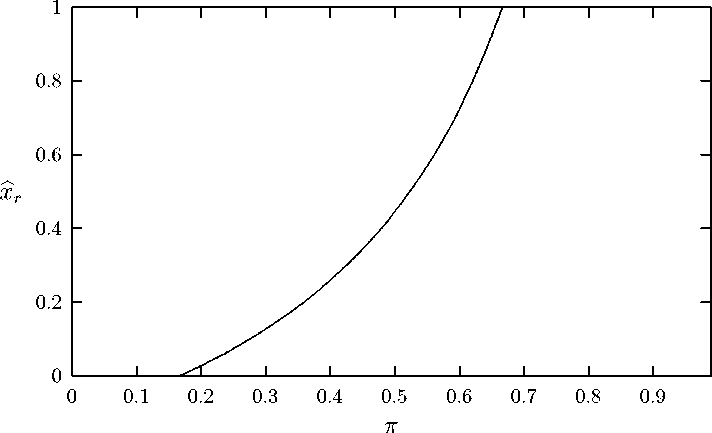

Lemma 3 For any π ∈ (0, 1), there exist Γo(π), Γ1 (π) such that for Γo(π) < Γ < Γ1 (π),

xbr (π) ∈ (0, 1) is the threshold level of stakeholder protection above which the incumbent

CEO’s entrenchment strategy becomes unprofitable. The threshold xbr is increasing in π and

Γ, and decreasing in ∆θ.

Proof. See the appendix. ■

Figure 2 depicts the function xbr (π) in the space (π, xr). Above the xbr (π) locus, the incum-

bent CEO never invests in stakeholder relationships. This is either because poor corporate

governance rules (low π) makes it easy for the CEO to preserve her job, or because explicit

stakeholder protection (xr high) makes stakeholders value less managerial concessions. In-

deed, when faced with a potential alliance with the incumbent management, stakeholders

trade off the benefit of managerial concessions against the cost of a less innovative manage-

ment: if they expect to receive a good treatment independently of who runs the firm, they

do not want to “strike” an implicit alliance with the incumbent CEO.

Figure 2: The function xbr .

Remark 1 The fact that the locus xbr (π) is increasing in π suggests that when stakeholder

activism is very effective, corporate governance reforms aimed at enhancing managerial

turnover should be accompanied by an increase in explicit stakeholder protection. If not,

they may simply spur more managerial concessions and stakeholder activism.

14

More intriguing information

1. The name is absent2. Standards behaviours face to innovation of the entrepreneurships of Beira Interior

3. Großhandel: Steigende Umsätze und schwungvolle Investitionsdynamik

4. The name is absent

5. Demographic Features, Beliefs And Socio-Psychological Impact Of Acne Vulgaris Among Its Sufferers In Two Towns In Nigeria

6. The name is absent

7. The Environmental Kuznets Curve Under a New framework: Role of Social Capital in Water Pollution

8. The name is absent

9. The name is absent

10. Expectations, money, and the forecasting of inflation